Second Quarter Highlights

- In April, U.S. Treasury (UST) yields surged higher in response to elevated inflation data but reversed some of that increase in May and June as economic reports softened.

- GDP growth moderated, with underlying components suggesting consumer and business demand is slowing. Personal consumption remains positive but has downshifted from the robust pace in prior quarters.

- The Federal Open Market Committee’s (FOMC’s) June fed funds rate projections were more hawkish than anticipated, with the new “dot plot” indicating just one cut to the policy rate over the balance of the year, compared to three cuts in the prior two dot plots.

- The ongoing resiliency of the economy — despite the aggressive actions of the Federal Reserve (Fed) over the last two years — has led to discussions within the FOMC that the longer-run neutral fed funds rate may be higher than previously assumed.

- Investment grade corporate issuance remained robust as total new supply year to date trails only the first-half pace of the pandemic-driven surge in 2020.

- Investment grade credit spreads were modestly wider during the second quarter but remain expensive relative to historical ranges.

- Interest rate volatility continued to moderate. The ICE BofAML MOVE Index, which measures implied rate volatility, dropped to the lowest level since the Fed first began tightening policy more than two years ago.

Duration Positioning

Neutral

Relatively neutral duration positioning given balanced yield and return symmetry.

Credit Sector

Slightly Overweight

Overweight Financials and select Industrial categories, namely the automotive and energy-related sub-sectors. Underweight Consumer Noncyclical, Capital Goods and Non-corporate Credit.

Structured Products

Overweight

Increased overweight positions in Asset-backed Securities (ABS) across strategies. Maintain overweight allocations in Agency Mortgage-backed Securities (MBS) across strategies.

2Q24: Progress is incremental

Benign economic data releases during the quarter diminished investor concerns of the potential for reaccelerating inflation. While the Fed acknowledged this progress, officials continued to emphasize the need for sustained and convincing disinflationary trends before rate cuts would be considered. Although labor markets remain healthy, a number of metrics indicate demand for workers is normalizing to more balanced levels. In response to these developments, fixed income yields moderated from year-to-date highs seen during the Spring, and interest rate volatility declined.

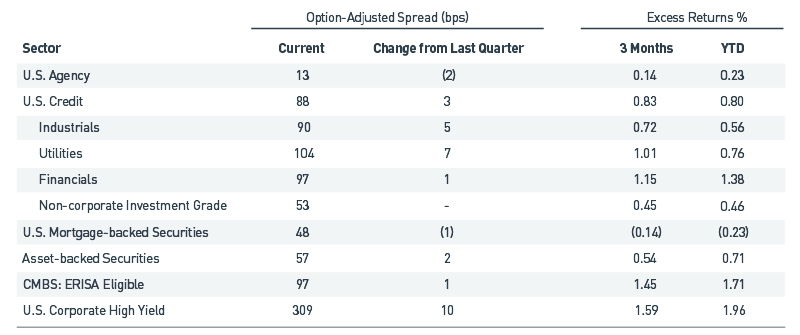

The Bloomberg U.S. Aggregate Index benefited from the higher yield environment, eking out a total return of 0.07% for the quarter despite an increase in rates of roughly 10-20 basis points (bps) across the yield curve. Credit spreads ended modestly wider, leading to a -0.03% excess return (Figure 1). The Financials sector outperformed other credit sectors for the third consecutive quarter, with an excess return of 0.23%. Structured product returns were mixed, as ABS outperformed and MBS modestly underperformed. Year-to-date returns within the high yield sector continue to outpace investment-grade performance.

Figure 1. Sector Comparison

Credit spreads widened modestly

As of 6/30/2024. Source: Bloomberg L.P.

Patience is paying off for the Fed

Economic data presented a conflicting narrative during the second quarter, with questions of whether the lagged effects of monetary policy were finally set to materialize. However, later in the quarter, inflation, labor markets and broad economic surveys began to trend slowly but consistently lower. After spiking early in the year, month-over-month increases in both the Consumer Price Index and Personal Consumption Expenditures Index steadily diminished. This gave the FOMC enough confidence to update its June meeting statement, declaring “modest progress” toward taming inflation versus the “lack of progress” from its prior statement. A more headline-worthy event for financial markets from the June meeting was the reduced median number of projected rate cuts for the balance of 2024, which declined from three to one. This forecast is hawkish relative to recent market pricing of more than two cuts.

Notably, both iterations of the FOMC’s 2024 dot plots have illustrated a slight increase in the longer-run neutral fed funds rate, rising to 2.75% from 2.50% at the beginning of the year. There has been an ongoing dialogue among Fed members in recent months about whether the longer-run fed funds rate has shifted higher in this post-pandemic environment. Chair Jerome Powell has acknowledged the potential upward shift in the equilibrium rate but downplayed its significance by emphasizing it is theoretical and does not guide current policy decisions. Importantly, Chair Powell and other Fed members believe the current policy stance remains restrictive. The resiliency of the current business cycle in the face of aggressive rate hikes has been striking, in our view, and increases uncertainty about the longer-run path of monetary policy.

While the Fed continues to preach patience to ensure recent inflation progress holds, other major central banks have shifted course. Both the European Central Bank and the Bank of Canada cut rates during the second quarter, with additional cuts anticipated later this year. The dollar has strengthened year to date as markets anticipate the United States will continue to have a higher interest rate environment than most other developed markets. Since the early stages of the pandemic, central banks have largely operated in unison, both in easing and then tightening policy. As their paths diverge, and contentious election cycles drive polarizing fiscal policy initiatives, renewed market volatility is likely.

F-V-T favors Structured Products over Credit

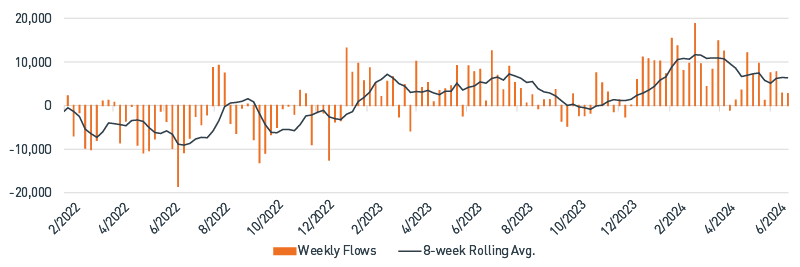

Swift investment-grade credit issuance continued in the second quarter, albeit at a slower pace than the record-breaking first quarter. The first-half of 2024 total of $867 billion in new supply trails only 2020, when issuers were rushing to primary markets to secure their balance sheets during the highly uncertain early days of the pandemic. Issuance is anticipated to slow in the second half of the year as some first-half activity was a function of companies pulling forward financing plans to capitalize on low risk premiums and strong investor demand. In addition, the pipeline of larger merger and acquisition-related issuance has been relatively muted. On the demand side, persistently positive inflows into fixed income products have absorbed the heavy supply, allowing valuations to grind lower over the course of the year (Figure 2). While these supply and demand dynamics look favorable in the near term, market technicals can be highly unpredictable, warranting caution at current valuations (Figure 3).

Figure 2. ICI Taxable Bond Long-term Mutual Fund and ETF Weekly Flows ($ millions)

Investor flows into fixed income products remain solid

As of 6/30/2024. Source: Bloomberg L.P., ICI

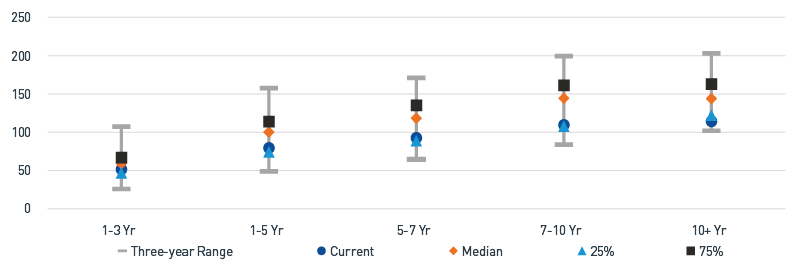

Figure 3. Bloomberg U.S. Credit Index, Historical OAS (bps)

Risk premiums in Credit remain expensive

As of 6/30/2024. Source: Bloomberg L.P.

Although credit fundamentals remain favorable, it will be interesting to see if some of the recent, softer economic data impacts upcoming second-quarter corporate earnings releases, or if it is conveyed through cautious forward guidance. Since higher inflation first appeared, we have favored corporate issuers with strong balance sheets and ample pricing power. At the same time, we have aimed to avoid industries and issuers that are more likely to be impacted by a higher-for-longer rate regime. Overall, our portfolio positioning continues to emphasize a high-quality bias.

With Credit valuations near the lower end of historical ranges, we continue to favor Structured Products, particularly the ABS sector as a higher-quality alternative. During the quarter, we continued to find attractive entry points, typically in new-issue markets, to increase exposure across all strategies. We executed this primarily through a rotation out of credit, where we continue to prune holdings that offer poor symmetry between potential risk and excess return.

Outlook: Fed shifts gears, risk assets stall out

Recent economic data supports the Fed’s narrative of at least one rate cut later this year — likely in September. Though still above the Fed’s long-run target, inflation trends have improved, and there is anecdotal evidence that companies are losing pricing power as consumers become more discerning. Both hard- and survey-based economic data have recently surprised to the downside, and expectations for second-quarter growth have drifted toward 1.5%. Finally, the edges of the job market are beginning to soften as the unemployment rate breached 4% and wage pressures eased.

The real policy rate remains highly restrictive. It could be the “long and variable lag” effects of the tightening campaign are finally beginning to emerge almost a year since the last hike. A relatively benign credit cycle supports rich valuations across both investment grade and high yield corporate bonds. We continue to find pockets of opportunity but mostly view Credit valuations as unattractive. Instead, we maintain a more defensive posture, focused on higher-quality and shorter-maturity segments of the market. Structured products, in our view, remain the most compelling overall relative value opportunity.

Over the first half of 2024, the excess return profile of ABS was double that of 1-3-year Credit, and we continue to see attractive pricing relative to lower-rated Industrials. Agency MBS has lagged other spread sectors and remains comparatively cheap. An expected shift in the Fed’s policy stance, combined with reduced volatility, may at last be the catalyst for consistent outperformance from the sector.

While markets seem well-behaved, certain risk factors, both domestically and globally, could be sources of volatility. Recent elections in Europe and Asia are putting pressure on the established leadership and rhyme with themes that may influence the upcoming U.S. presidential contest. Geopolitical tensions remain elevated, and policy issues such as immigration and tariffs may have material impacts on growth and inflation. At the same time, we continue to accumulate record peacetime U.S. fiscal deficits that will exert additional strain on the upcoming budget cycle.

Optimizing the reward/risk profile of our clients’ portfolios is our perennial objective. Quiescent risk environments can persist for extended periods, such as from 2004 through mid-2007 and much of 2021, which keeps us mindful of our risk posture, as opportunities for outperformance in environments with more modest excess return expectations may be limited. Excluding the agency MBS sector, we believe meaningful spread compression is unlikely, and at best, we expect markets to produce excess returns consistent with carry. When confronted with these dynamics, we continue to find that a good defense can be the best offense and believe our up-in-quality and Structured Product bias has — and will — reward our clients over the long term.

Important Disclosures

Index definitions are available at https://www.pnccapitaladvisors.com/index-definitions/

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

©2024 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE