First Quarter Highlights

- Robust labor markets and firmer-than-anticipated inflation data resulted in an upward shift in U.S. Treasury (UST) yields during the first quarter.

- While the Federal Open Market Committee (FOMC) maintained the target fed funds rate range at 5.25%-5.50%, officials continued to indicate possible rate cuts later this year.

- During his post-FOMC press conference, Chair Jerome Powell kept his comments on the Federal Reserve’s (Fed’s) balance sheet strategy high level but did indicate that it will be appropriate to slow the pace of runoff soon.

- Market expectations for rate cuts have adjusted significantly since the end of 2023. At quarter end, implied market pricing indicated roughly three cuts for the balance of 2024; however, recent inflation data has pushed the first cut out until September and trimmed expectations for cuts to less than two.

- Despite setting a new first quarter record for corporate issuance, insatiable investor demand allowed new supply to be easily absorbed, creating an environment for credit spreads to grind lower during the quarter.

- Relative value opportunities remain somewhat limited within Corporate Credit. While Financials and shorter-dated maturities remain modestly attractive on a historical basis, we continue to find more compelling opportunities in higher-quality alternatives within the Structured Products sector.

Duration Positioning

Near Neutral

Relatively neutral duration positioning given favorable yield and return symmetry.

Credit Sector

Modestly Overweight

Overweight Financials and select Industrial categories, namely the Automotive and Energy-related sub-sectors. Underweight Consumer Non-cyclical, Capital Goods and Non-corporate Credit.

Structured Products

Overweight

Maintaining overweights in Asset-backed Securities (ABS) across short and intermediate strategies. Remain overweight in Agency Mortgage-backed Securities (MBS) across styles.

Post-pivot Reality Check

The impressive UST rally during the last two months of 2023 ran out of steam during the first quarter as economic data persistently exceeded expectations. By the end of March, roughly half of the fourth-quarter drop in yields reversed, with yields rising approximately 30-40 basis points (bps) across the curve.

Fed policy continued to dominate the fixed income market narrative during the quarter. While the Fed continued to communicate a desire to ease policy at some point in 2024, stubborn inflation and a seemingly invincible labor market pushed expectations for rate cuts largely to the back half of the year. Unlike several prior instances over the last couple years, rising UST yields did not catalyze risk-off market conditions during the first quarter. Rather, equity markets surged to new heights, and credit spreads fell to levels last seen during the zero-rate policy years of 2020-2021.

The increase in rates resulted in a -0.78% total return for the Bloomberg U.S. Aggregate Index. Improved income return helped largely offset price declines from higher rates. Credit spreads compressed 8 bps, generating a positive excess return of 0.83% (Figure 1). After languishing behind Industrials and Utilities for much of 2023, Financials materially outperformed during the first quarter, with a positive excess return of 1.15%. It was a mixed story in Structured Products; ABS enjoyed a strong quarter with excess returns of 0.54%, while MBS underperformed and was the only sector with negative excess returns.

Figure 1. Sector Comparison

Spread compression enabled positive excess returns during the quarter

As of 3/31/2024. Source: Bloomberg L.P.

Economic Data Throws Cold Water on Rate Cuts

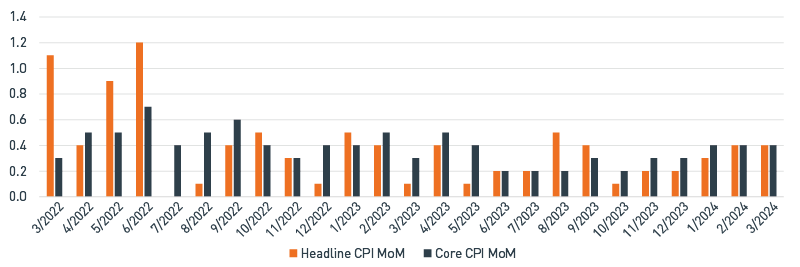

At the end of December 2023, implied market pricing discounted more than six cuts to the fed funds rate over the course of 2024. However, recent economic data has forced the market to reset its sights lower. The March labor report exceeded expectations by virtually all measures as nonfarm payrolls increased by 300,000 net new jobs, alongside upward revisions to already solid prior months. The unemployment rate ticked lower to 3.8%, while average hourly earnings remained quite firm, with continued year-over-year wage growth above 4%. It was a similar story on the inflation front with continued hotter-than-anticipated data. Recent trends in the core Consumer Price Index (CPI) have been particularly concerning as several month-over-month (MoM) changes of 0.4% are well above the pace of increases during the second half of last year (Figure 2).

Figure 2. CPI, % change MoM

Recent, incremental upticks in inflation demonstrate staying power

As of 4/10/2024. Source: Bloomberg L.P.

Fed messaging about the future path of monetary policy has remained steadfast, despite the vacillating expectations of the market. Officials remain consistent: they need to obtain a greater level of confidence that inflation is moving sustainably toward 2% before initiating policy rate cuts. Progress against inflation has been more evident in the Fed’s preferred measure, the Personal Consumption Expenditure Index, due to the composition of its sub-categories. However, broader economic surveys suggest additional headway may be harder to come by in the coming months, and recent hawkish comments from Fed officials echo this sentiment. Markets have increasingly come to grips with the Fed’s “higher-for-longer” mantra on interest rate policy. While real yields in the U.S. Treasury Inflation-Protected Securities market are at the upper end of recent ranges, thus far risk markets have remained resilient.

The March FOMC announcement failed to address any potential changes to the pace of the Fed’s balance sheet reduction program. However, Chair Powell indicated in his post-meeting press conference that it would be appropriate to slow the pace “fairly soon.” He also signaled the longer-run goal is to return holdings back to being mostly composed of Treasuries but expressed no urgency in reducing the roughly $2.4 trillion in current MBS holdings. March meeting minutes provided more insight, indicating most participants favored tapering the monthly pace by roughly half, with a focus on Treasury holdings. We believe this topic will continue to garner more attention and could become a priority should funding pressures emerge across financial markets. To date, the roughly $1.5 trillion in total balance sheet reductions has not impacted liquidity conditions in funding markets. With money market assets exceeding $6 trillion, the Fed has been able to reduce its reverse repo balances to under $500 billion as the U.S. Treasury ramped up bill issuance.

Sector Positioning: Juice Not Worth the Squeeze

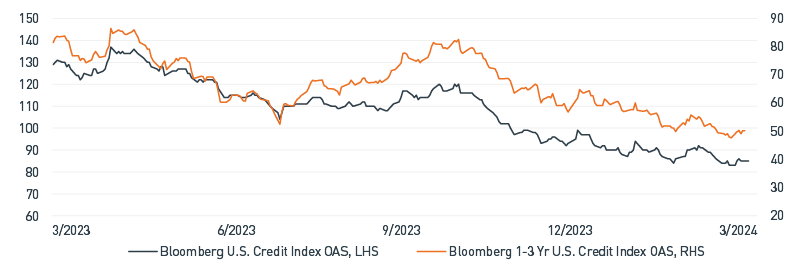

Unlike the Treasury market, credit spreads continued to rally during the first quarter — an achievement all the more remarkable in the face of record first quarter new issuance that exceeded $500 billion. Investor demand was strong as new issue concessions were generally minimal, and most deals were well over-subscribed. Modest indigestion was evident during late February as more than $200 billion was issued during the month, including several blockbuster deals driven by acquisition-related funding. Reduced supply in March then paved the way for spreads to grind lower toward levels last seen in late 2021 (Figure 3).

Figure 3. Bloomberg U.S. Credit Index vs. Bloomberg U.S. Credit 1-3 Yr Index, avg.

Option-adjusted Spread (OAS), bps

Spreads continued to grind lower, reflecting strong economic conditions

As of 3/31/2024. Source: Bloomberg L.P.

In general, risk premiums have been supported by the surprising resiliency of the economy and underlying credit fundamentals. Corporate earnings growth remains solid as most industries have maintained profit margins by passing through price increases to customers. Likewise, investor sentiment remains highly optimistic. Recession fears have waned, and confidence around anticipated productivity gains associated with artificial intelligence continues to stoke animal spirits. We remain attentive to risks from persistent inflationary pressures and potential escalation in geopolitical tensions that could result in a shift in sentiment.

Opportunities are more apparent in Structured Products, where we maintain overweight allocations within ABS. Despite strong performance in the first quarter, valuations remain attractive relative to other short-duration alternatives. While credit trends have slightly deteriorated to more normalized levels, strong labor markets continue to support prime borrowers. Similar to credit markets, new issuance was robust during the first quarter but was easily absorbed by investors, providing a strong technical backdrop that appears likely to continue.

Outlook: Boring is Brilliant

Historical spread relationships suggest the symmetry of potential excess returns in credit are modest at best. As such, we have used the placid environment during the last several months to reduce overall portfolio risk profiles. While we remain overweight within Corporate Credit, our overall positioning is more balanced when factoring in the higher-quality Non-corporate sector, where we remain underweight. Given relatively expensive spread levels, we believe the opportunity cost of this defensive posture is lessened, particularly as we pursue a more tactical approach. History suggests that the lagged effects of policy tightening can surface quickly and without warning. So, while we maintain a positive view on the economy, we continue to tread lightly in riskier sectors until more favorable opportunities emerge.

Although interest rate volatility began to moderate in the first quarter, economic data suggests the Fed will need to maintain a more restrictive policy stance over the coming months. Despite strong growth, the U.S. government continues to run considerable budget deficits that will necessitate ongoing refunding needs. At the same time, geopolitical tensions remain high and have the potential to quickly escalate. These are market environments in which a good defense can be the best offense. We have demonstrated an ability to navigate challenging conditions, limiting portfolio volatility and driving consistent excess returns across our strategies. Our disciplined approach and track record have been recognized by PSN, most recently awarding our Short Duration 1-3 Year strategy the distinction of Manager of the Decade.

Heightened levels of interest rate volatility have been one of the most consistent themes since the Fed embarked on its monetary policy tightening campaign two years ago. During the first quarter, that trend began to reverse course as rate volatility steadily subsided. However, we believe the reversal will be short-lived as the uneven nature of the disinflation process seems likely to persist. Coupled with troublesome federal deficits that are unlikely to be addressed heading into a presidential election, choppy Treasury auctions remain an additional wildcard as a source for episodic volatility. While renewed rate volatility does not always carry over to broader financial markets, when risk premiums are fully valued, as they are today, we believe a patient approach is warranted.

Important Disclosures

Index definitions are available at https://www.pnccapitaladvisors.com/index-definitions/

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

©2024 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE