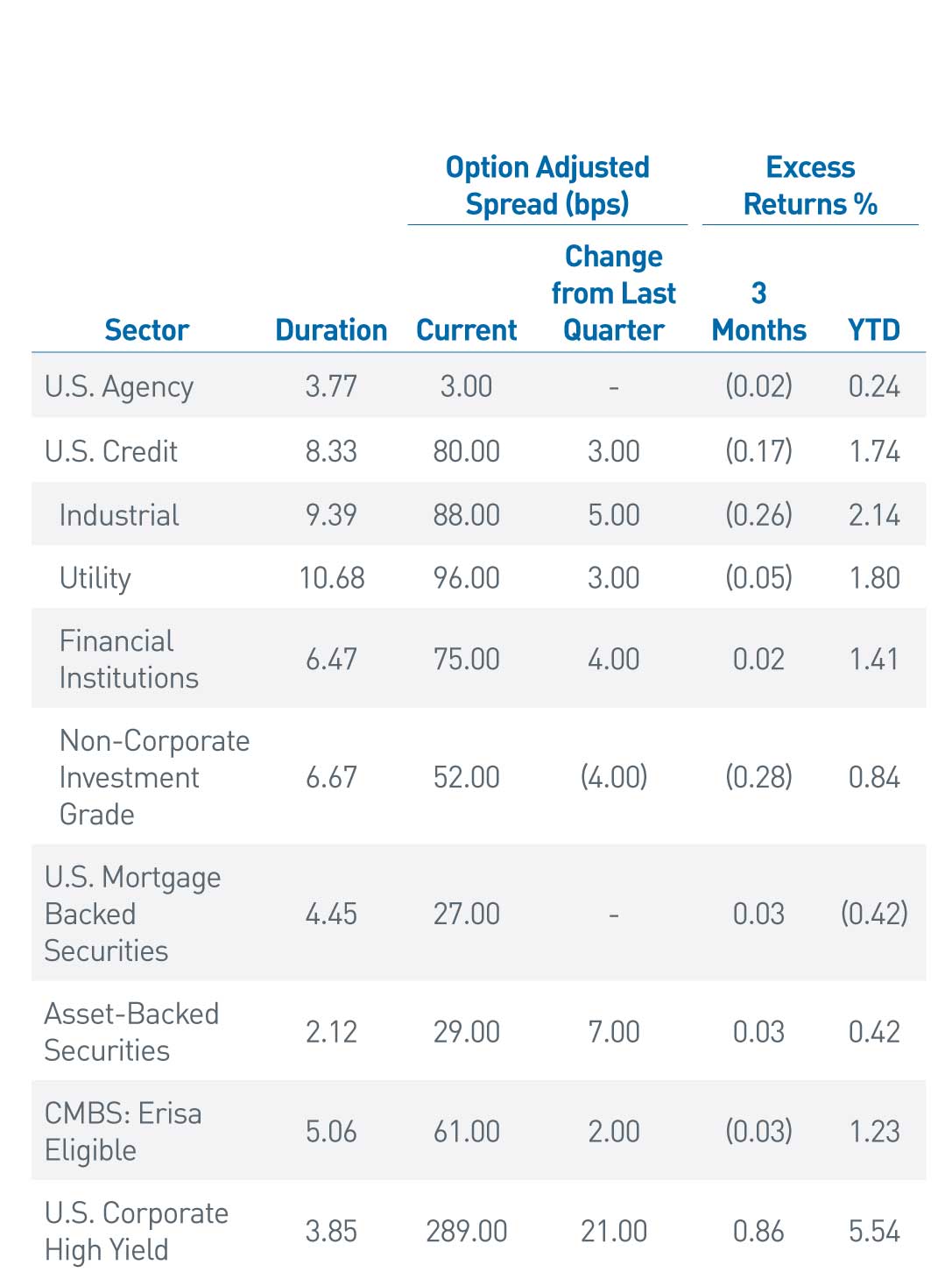

Sector Review

Despite plenty of attention-grabbing headlines and conflicting economic data, fixed income markets were generally calm during the third quarter as interest rates and risk premiums closed the quarter about where they started. The Fed continued to be front and center as it prepared to adjust its balance sheet strategy, while uncertainty regarding the direction of fiscal policy initiatives intensified due to partisan divides. Similar to the fourth quarter of last year, markets looked past a surge in COVID-19 cases and focused on the continued but slowing economic recovery. Consequently, the Bloomberg Aggregate Index realized a total return of just 0.05% for the quarter. Investment grade excess returns were mixed among sectors during the quarter, generating a negative 0.17% of excess returns (Figure 1). Year to date, Agency MBS continues to lag other sectors with cumulative negative excess returns.

Figure 1. Sector Comparison

Macroeconomic headwinds led to negative excess returns in key sectors.

As of 9/30/21. Source: Bloomberg L.P.

Central Bank Ornithology

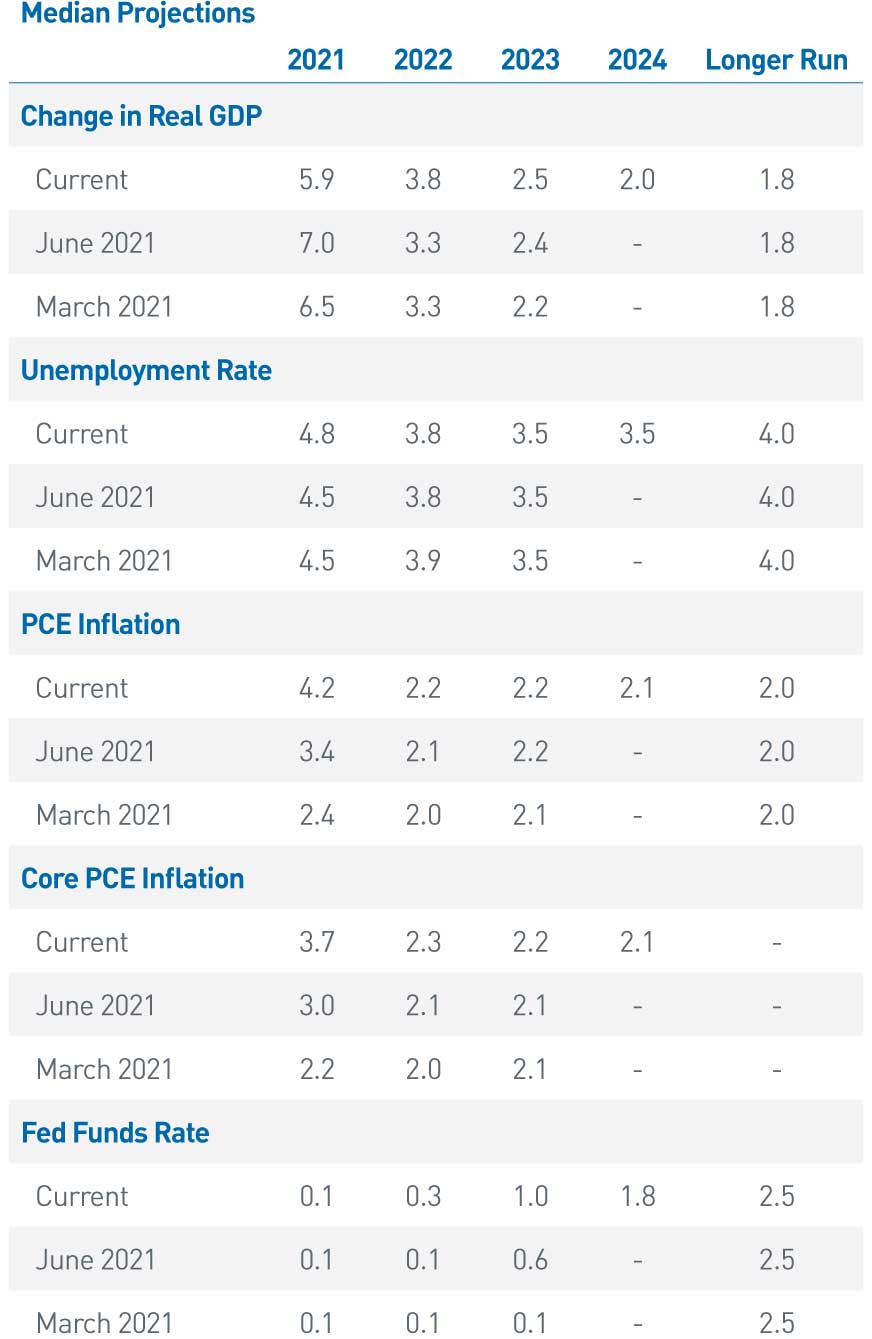

The FOMC took another step towards less accommodative monetary policy during its September meeting as the committee’s statement indicated “a moderation in the pace of asset purchases may soon be warranted” if progress continues toward the Fed’s labor and inflation objectives. Chair Powell elaborated during his press conference that the tapering of asset purchases could commence in line with the Fed’s next meeting in November and conclude by mid-2022. This timing is modestly more hawkish than expected but consistent with statements by several Fed members leading up to the meeting. Updated federal funds rate projections also garnered attention as the median year-end forecast for 2022 and 2023 rose to 0.25% and 1.0%, respectively, up from 0.125% and 0.625% in June. These adjustments correspond to the Fed’s new economic projections, specifically around inflation expectations, which once again were revised significantly higher (Figure 2).

Central bank policy was not the only issue that garnered headlines for the Fed during the quarter. The presidents of the Federal Reserve Bank of Dallas and Boston attracted criticism for personal trading activity in 2020, revealed through required annual disclosures.

Senator Elizabeth Warren had a “trading tantrum” in a series of speeches and indicated she was “Fed Up” with Chair Powell’s leadership and would not support his reappointment. Both presidents, Robert Kaplan and Eric Rosengren, bowed to pressure and resigned in late September. Other potential vacancies may arise through retirements and term expirations which could shift the balance between perceived hawks and doves heading into a pivotal period for policy and the economy. Chair Powell’s own term expires in February, and while still favored for renomination, President Biden has not offered a clear endorsement as he weighs concerns from more progressive factions of the Democratic party. At a minimum, developments related to the Fed and its policy decisions will remain a primary driver of financial markets in the coming months.

Fiscal Policy Initiatives Face a Cliff

High levels of uncertainty regarding tax and spending policies persist despite the legislative majorities held by Democrats. While the probability of a large-scale partisan reconciliation bill fades, seemingly so do the prospects for the bipartisan infrastructure bill as well, further deepening divides in D.C. This looms ominously for round two of the debt ceiling battle, which has now been pushed into early December from mid-October. The impact on markets was generally muted heading into the original deadline of Oct. 18, with only modest increases in similarly dated UST bill yields. Given recent dynamics in Congress, it seems likely for these negotiations to again come down to the wire, potentially becoming a source of market volatility.

Tran•si•to•ry (adjective): Not Permanent

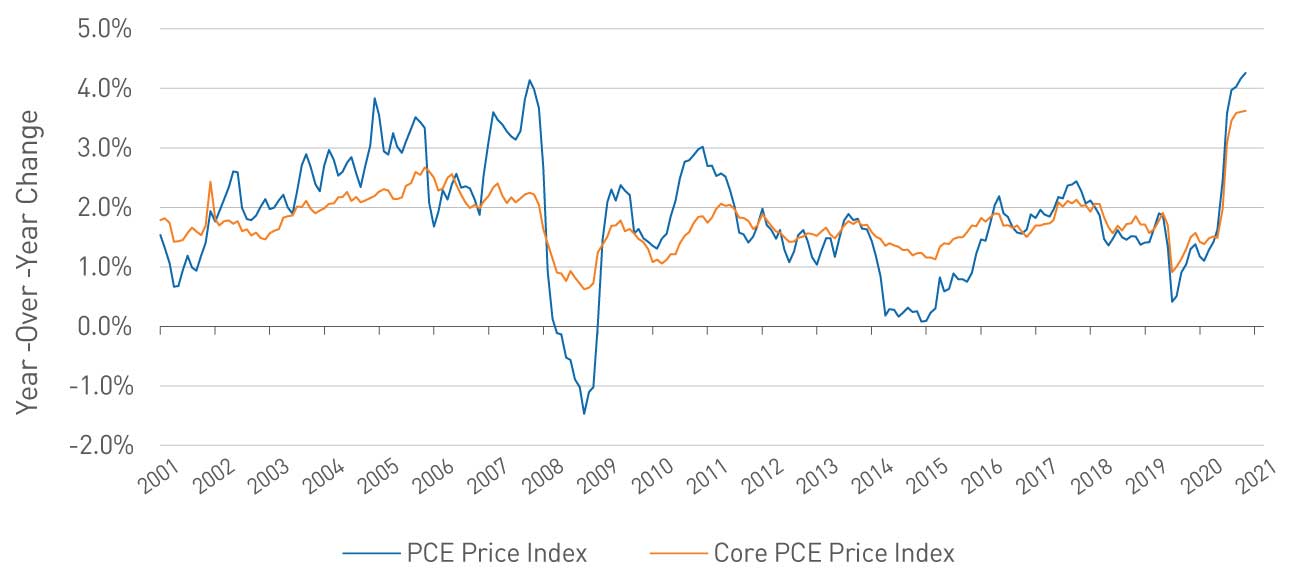

Recent reports indicate the inflation rate has risen to a 13-year high of 5.4%. It continues to run well above the Fed’s 2.0% target as raw material shortages, supply chain disruptions and an extensive lack of labor continue to pressure prices higher given solid consumer demand (Figure 3). In conjunction with the Fed’s September update to the Summary of Economic Projections, the central tendency was revised higher by nearly 100 basis points (bps) for 2021. Rising commodity and energy prices over recent weeks could add additional pressure heading into the winter heating season. While these forces could still prove transitory, they have persisted beyond most expectations and have contributed to a general uneasiness, particularly in businesses with weaker pricing power. Near-term growth expectations have cooled as these disruptions have pushed some consumption into the future, with auto sales being one of the most identifiable examples. Should these issues persist it’s possible some degree of demand destruction takes place, further weighing on growth prospects.

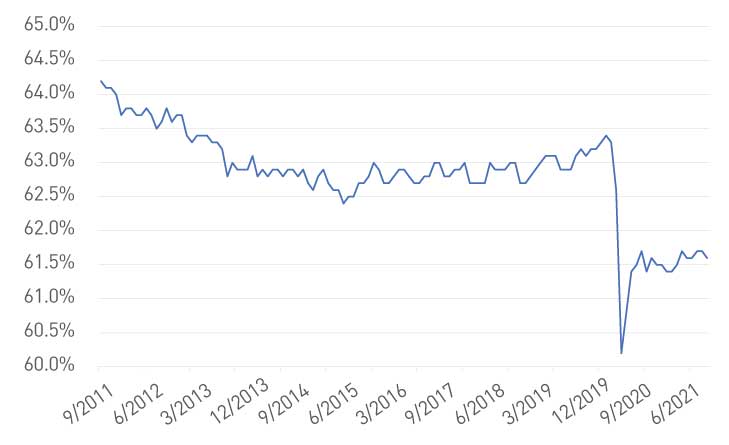

Wage growth continues to be elevated but to date has done little to close the gap in job openings as the labor participation rate remains well below pre-pandemic levels (Figure 4). The September payroll report demonstrated this dynamic as the headline number missed expectations by a wide margin for the second straight month, yet the unemployment rate plunged 0.4% to 4.8%. Similar perplexing economic data seem likely to continue as the global economy attempts to find a new normal. This will continue to challenge policy makers and keep the risk of a potential policy error elevated.

Figure 2. Summary of FOMC Economic Projections

Inflation estimates were revised higher once again.

As of 9/30/21. Source: U.S. Federal Reserve

Figure 3. Personal Consumption Expenditure (PCE) Indices

A number of factors continue to pressure prices higher.

As of 9/30/21. Source: FactSet® . FactSet® is a registered trademark of FactSet Research Systems, Inc. and its affiliates.

Outlook: Markets Barely Shaken, Not Deterred, but Headwinds Beginning to Blow

During the quarter, credit markets were generally tranquil, while equities softened from all-time highs. Corporate bond spreads continued to exhibit minimal volatility and remain expensive in a historical context. As we discussed in a recent commentary, this environment requires a thoughtful approach toward incorporating credit into portfolios. Over the course of 2021, we modestly reduced overweights in intermediate and core styles given the asymmetry of returns in longer-duration credit. Conversely, in shorter-duration strategies, we have added exposure by capitalizing on relatively steep credit curves in the front end fostered by strong investor demand for alternatives to low-yielding cash alternatives.

Outside credit, we have maintained underweights to Agency MBS in aggregate strategies; we await more attractive opportunities to present themselves as the Fed begins to taper its purchases or a renewed bout of interest rate volatility takes hold. Our use of Treasury Inflation-Protected Securities continues to be tactical in nature as we look to opportunistically use the sector when it displays favorable carry profiles.

U.S. financial markets have shown tremendous resiliency in the face of significant challenges, from the evolution of domestic monetary and fiscal policy throughout the pandemic to international geopolitical risks, such as concerns currently emanating from an arguably overextended property market in China. For much of the last six months, headlines from China have turned negative and increasingly authoritarian as the government wrestles with rising socioeconomic inequalities. The downside risks posed by a shock to the Chinese economy creates yet another potential growth headwind entering the fourth quarter.

Figure 4. U.S. Labor Force Participation Rate

Labor participation remains well below pre-pandemic levels.

As of 9/30/21. Source: Bloomberg L.P.

We believe there is a degree of complacency in markets given fully priced valuations in riskier assets in the face of some unique challenges that seem likely to persist. We see potential downside risks across the four primary factors we evaluate to frame our market outlook — monetary policy, fiscal policy, inflation and volatility — which supports more defensive portfolio positioning. Seeking to ensure our clients are adequately compensated for risks arising from our sector allocation decisions is a core element of our investment process. Being patient in the face of conflicting data and rising headwinds seems most prudent at this juncture.