Macro

June economic data releases started off strong with a robust jobs report that significantly exceeded consensus expectations. However, unemployment ticked higher to 4.0%, the highest rate since January 2022. Additionally, wage growth proved stronger than expected and remains above the Federal Reserve’s preferred level. Despite signs of cooling, the labor market, in our view, remains resilient overall.

As widely expected, the Federal Open Market Committee (FOMC) kept rates unchanged at its June 12 meeting. The closely monitored “dot plot” reflected a median expectation for one rate cut in 2024. Notably, FOMC participants raised their expectation for Personal Consumption Expenditures growth, their preferred inflation measure, to 2.8% from 2.6%. In his post-meeting press conference, Chair Jerome Powell once again acknowledged the persistence of inflation and that it is “taking a bit longer” to gain confidence it is slowing.

Credit

Issuance for June exceeded expectations, closing the month with slightly more than $100 billion in new supply. Forecasted issuance for July approximates $80 billion, which, if accurate, would represent the slowest monthly pace of the year.

Overall, the pace of investment grade issuance through the first half of 2024 trails only the record issuance of the pandemic-era, first half of 2020. Investment grade issuance through June 30, 2024, tallied $867 billion, versus $1.2 trillion through the same period in 2020.

Credit spreads widened 8 basis points during June, making valuations modestly more attractive relative to recent levels.

Structured

The asset-backed securities sector softened during June as the market absorbed new supply, which is now running approximately 32% ahead of supply at this time last year.

Mortgage-backed securities outperformed other risk assets during the month, with episodes of widening spreads interpreted as attractive entry opportunities.

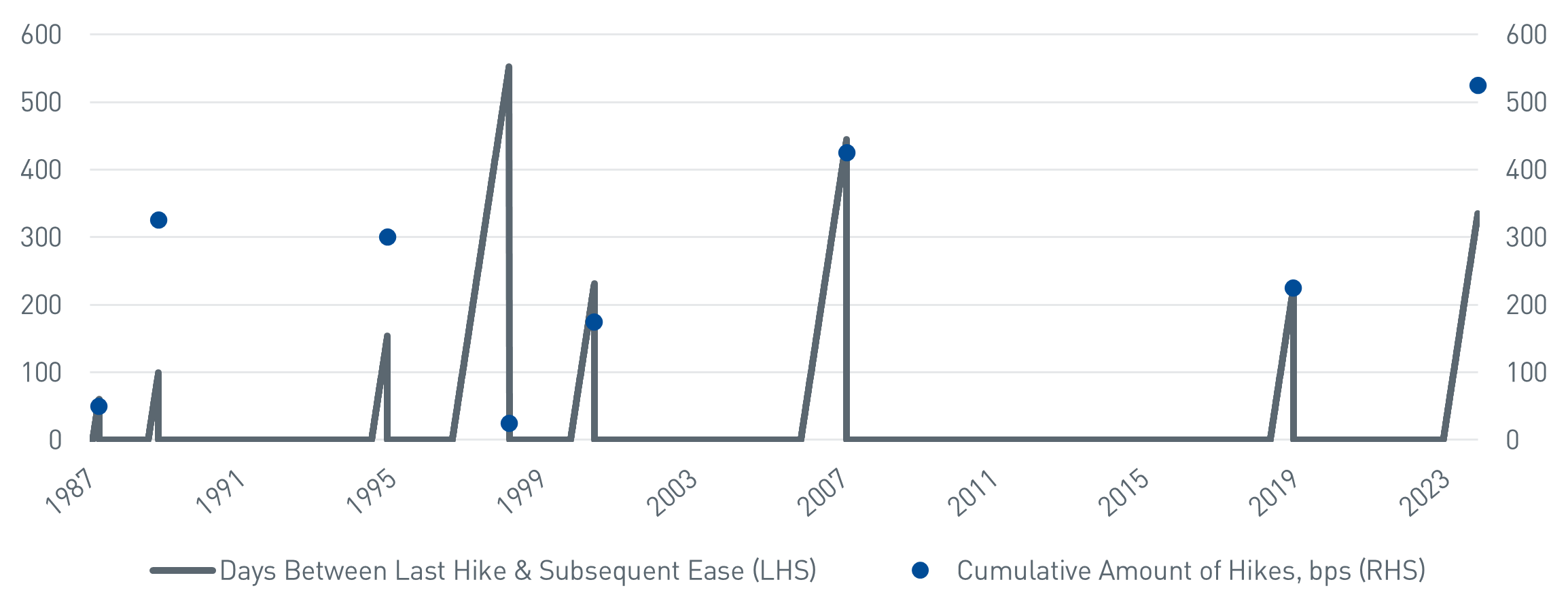

Chart of the Month: Federal Reserve Tightening Cycles

- The Federal Reserve has been “on pause” for almost a year, a relatively long time considering the degree of tightening that has occurred in this cycle.

As of 6/28/2024. Source:

Bloomberg L.P.

Market Data

As of 6/28/2024. Source:

Bloomberg L.P.

Bloomberg Sector/Index Performance (USD)

As of 6/28/2024. Source:

Bloomberg L.P.

Important Disclosures

This publication is for informational

purposes only. Information contained herein is believed to be accurate, but has

not been verified and cannot be guaranteed. Opinions represented are not

intended as an offer or solicitation with respect to the purchase or sale of

any security and are subject to change without notice. Statements in this

material should not be considered investment advice or a forecast or guarantee

of future results. To the extent specific securities are referenced herein,

they have been selected on an objective basis to illustrate the views expressed

in the commentary. Such references do not include all material information

about such securities, including risks, and are not intended to be

recommendations to take any action with respect to such securities. The

securities identified do not represent all of the securities purchased, sold or

recommended and it should not be assumed that any listed securities were or

will prove to be profitable. Past performance is no guarantee

of future results.

Indices and/or Benchmarks Definitions

PNC Capital Advisors, LLC is a

wholly-owned subsidiary of PNC Bank, National Association, which is a Member

FDIC, and an indirect subsidiary of The PNC Financial Services Group, Inc.

serving institutional clients. PNC Capital Advisors› strategies and the

investment risks and advisory fees associated with each strategy can be found

within Part 2A of the firm's Form ADV.

PNC Capital Advisors, LLC claims

compliance with the Global Investment Performance Standards (GIPS®). A list of

composite descriptions for PNC Capital Advisors, LLC and/or a presentation that

complies with the GIPS® standards are available upon request.

Investments: Not FDIC Insured. No Bank

Guarantee. May Lose Value.

©2024 The PNC Financial Services Group,

Inc. All rights reserved.