Fundamentals, Valuations and Technicals keep us moored in choppy seas

With a recession in the offing for the back half of this year, coupled with the potential for an own goal if debt ceiling negotiations flatline, we believe markets remain susceptible to episodic volatility. In this environment, we believe the best offense is good defense, underpinned by our risk-focused investment process.

We are amid the most aggressive Federal Reserve (Fed) monetary policy tightening regime in 40 years, after nearly 15 years of near-zero interest rates, also a historical record. Unfortunately, the velocity of change has left some areas of the market with interest rate whiplash. While the Fed’s rate raising may have reached a zenith with its latest increase in early May, to a range of 5.00% - 5.25%, it is not a foregone conclusion.

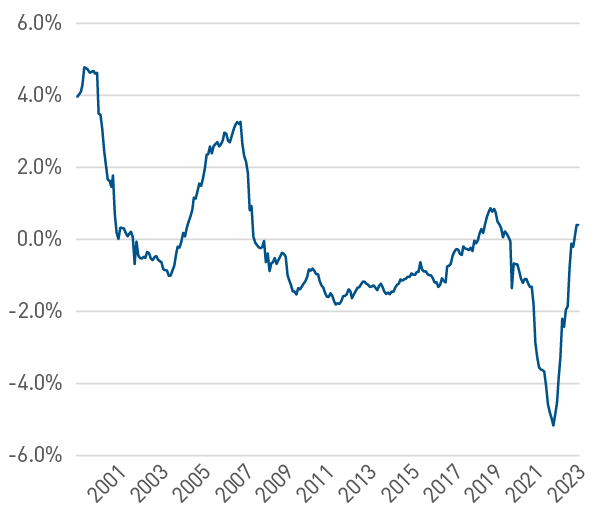

The target of the Fed’s ire — stubbornly high inflation — is on a downward trend but remains well above its 2% long-term goal. While the headline Consumer Price Index edged below 5% in April, the real fed funds rate has only recently crossed into positive territory (Figure 1). Meanwhile, labor markets show continued strength, consumer spending is steady and housing activity is improving. As a result, the second quarter Atlanta Fed GDPNow forecast is trending toward a solid 3%.

Figure 1. Real Fed Funds Rate

The real fed funds rate just recently turned positive

As of 4/30/2023. Source: Bloomberg L.P.

Despite the data, investors continue to seem willing to fight the Fed. While the Fed remains committed to keeping policy rates higher for longer, at least through the end of this year, the fed funds futures market is predicting rate cuts as early as the third quarter. Unless there is evidence of sustainable progress on inflation and a material shift in labor dynamics, we believe the market continues to underappreciate the Fed’s resolve.

Charting our course

Navigating markets amid this “great reset” is a test of investor fortitude. For us, the pillars of our investment process help us avoid the pitfalls of market extremes, but they also help uncover opportunities in times of turbulence.

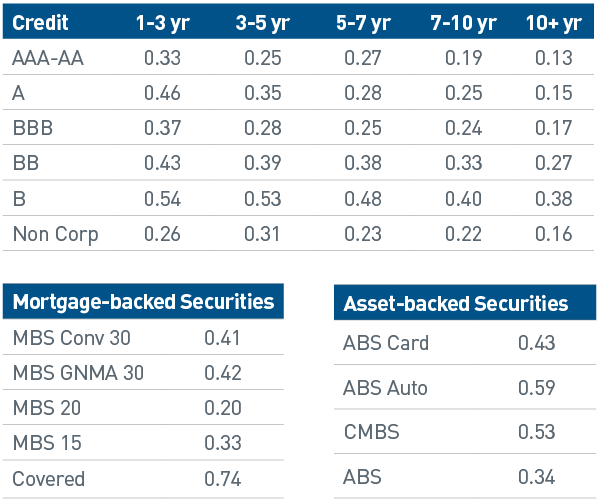

Currently, we are finding opportunities in sectors that our research has shown historically demonstrate attractive risk-return characteristics. One metric we review regularly is the modified information ratio (MIR). MIRs measure excess returns relative to the annualized volatility of those excess returns, resulting in a standardized measure we can compare across sectors (for a detailed discussion of MIRs and how we employ them, see our paper, “Optimizing Risk-Return Outcomes in Core Fixed Income”).

In Figure 2, we substitute current sub-sector option-adjusted spreads (OAS) into the analysis as a simplified view of potential forward excess returns.

Figure 2. Comparison of Current MIRs

Valuation discounts may present compelling opportunities

All data for the period March 2018 to April 2023. MIRs calculated by dividing current option-adjusted spreads over the period by Annualized Volatility. Annualized volatility calculated by multiplying the monthly standard deviations by √12. Source: ICE BofA US Broad Market Index series, PNC Capital Advisors

Within corporate credit, short-duration A-rated securities screen favorably, due in part to discounts associated with Financials as recent banking industry challenges are synthesized by the market. From a historical perspective, the valuation gap between Financials and Industrials is quite stark.

Banking industry fundamentals appear largely sound, with solid capital positions, healthy balance sheets and strong liquidity, a few bad actors aside. Given our focus on fundamentals in the context of the macroeconomic environment, we believe current valuation discounts present a compelling opportunity. We have continued to add modestly to our Financials overweight, with a focus on systemically important financial organizations and on large regional banks to a lesser extent. We favor organizations with significant scale as they are subject to more rigorous oversight and maintain more diversified business models.

Asset-backed security MIRs have been elevated since late 2022 and continue to screen positively, particularly when compared to corporate investment-grade alternatives. In our view, AAA-rated 2 to 3-year new issue tranches are attractive, as recent deals priced with a notable yield pick-up versus A-or-better-rated Industrials with similar maturities. In our view, investors continue to demonstrate a clear preference for high-quality, non-financial Corporates and are assigning a discount to asset-backed securities, due in part to the underlying finance receivables that support the structures.

Finally, 30-year agency mortgage-backed securities appear attractive relative to similar duration corporates. We maintain a modest overweight to the sector but remain cognizant of ongoing technical headwinds. While origination supply has moderated due to higher mortgage rates and slower housing market activity, bank demand has waned due to sector stress. Additionally, both the Fed and the Federal Deposit Insurance Corporation have been net sellers.

We still believe there is considerable opacity in the outlook and feel a good defense is the best offense. While our positioning is conservative, we are overweight select sub-sectors of risk assets that we believe offer compelling return symmetry and that have historically shown strong risk-return outcomes.

Important Disclosures

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

©2023 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE