Fourth Quarter Highlights

-

Financial markets remain optimistic that significant monetary and fiscal support can provide sufficient economic stability until widespread vaccine dissemination occurs.

-

Credit spreads continued to tighten over the course of the 4Q, ending the year at valuations similar to pre-Covid levels.

-

The Federal Reserve (Fed) strengthened their commitment to accommodative policy with guidance that their asset purchase strategy will continue at its current pace until substantial further progress is achieved on both their employment and inflation objectives.

-

At their December meeting the Fed expressed limited interest in adjusting the composition of their balance sheet holdings, likely leaving this in their toolkit should economic or market conditions deteriorate.

-

Additional fiscal stimulus and election results that consolidated executive and legislative control with Democrats has led to a steepening US Treasury (UST) curve and expectations for a reflationary environment in 2021.

-

Volatility measures continue to be well contained and financial conditions remain highly favorable.

Duration Positioning

Neutral

Continue to maintain a benchmark-like duration stance across strategies.

Credit Sector

Overweight: Reducing exposure across strategies

Overweight Financials and select Industrial sectors, primarily focused in the energy and cyclical sub-sectors, continue to emphasize shorter duration maturities. Remain significantly underweight the Non Corporate credit sector.

Structured Products

Neutral in aggregate strategies; Overweight in short duration strategies

Modestly reduced overweight's in Asset-Backed securities while maintaining Agency Mortgage-Backed Security allocations.

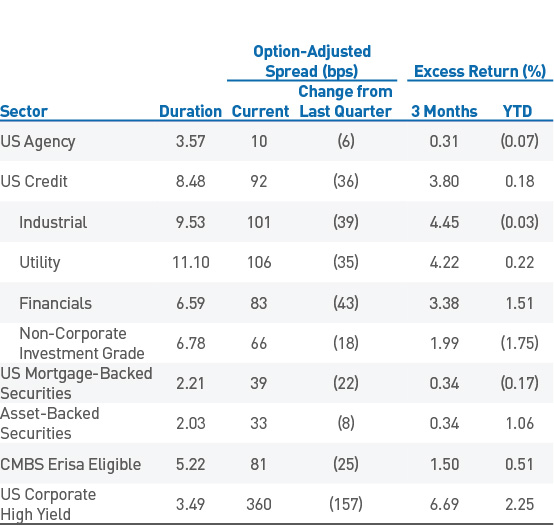

Fourth Quarter Sector Review

The recovery in financial markets picked up steam in the fourth quarter as investors continued to rotate into riskier sectors given an insatiable desire for incremental yield. Market risk appetites were fomented by resolution of several notable concerns: election results, additional fiscal stimulus’ and viability of several vaccines to combat the on-going pandemic. The Bloomberg Barclays Aggregate Index produced a positive total return of 0.67% for the quarter and 7.51% for the year. Positive returns for the quarter were attributed to spread compression across most sectors totaling 1.34% in excess returns, which offset the negative performance impact of rising UST rates across much of the yield curve. US Credit again was the star performer as the Bloomberg Barclays US Aggregate Credit index tightened by 36 bps, which generated 3.80% in excess returns for the quarter. This impressive rally helped the credit sector completely offset the 1Q sell off, pushing excess returns into positive territory for the year. It was a similar story in high yield markets with the Bloomberg Barclays US Corporate High Yield index generating 6.69% excess return for the quarter. High-quality structured products saw more muted positive excess returns of 0.34% for both the Asset-Backed and Agency MBS sectors.

Monetary & Fiscal Policy Remain the Primary Drivers of the Recovery

The Fed continues to reinforce that they will maintain their current policy stance into the foreseeable future. At the December Federal Open Market Committee meeting they announced that they will maintain the current pace of their asset purchase program “until substantial further progress has been made towards the Committee’s maximum employment and price stability goals.” The Fed deferred on changing the maturity profile of its holdings and now some market participants (as well as Fed officials) have shifted their focus to the timing of potential tapering of the balance sheet program. Chair Jerome Powell indicated that interest rate sensitive sectors such as the housing market are healthy and financial conditions remain highly accommodative suggesting a limited interest in terming out the maturities of asset purchases absent any material deterioration in these important metrics. While economic data continues to firm and inflation measures have recovered substantially, it appears highly likely the Fed will be proceeding with the $120bn per month pace of purchases for some time. Powell has also indicated that the expected uptick in yearly inflation rates in the coming months (given the steep drops in 1Q20) are likely to be transitory. This should provide the Fed sufficient flexibility to continue supporting the economy despite possible concerns on inflation, which is consistent with the updated framework that was provided last summer.

As of 12/31/20. Source: Bloomberg Barclays

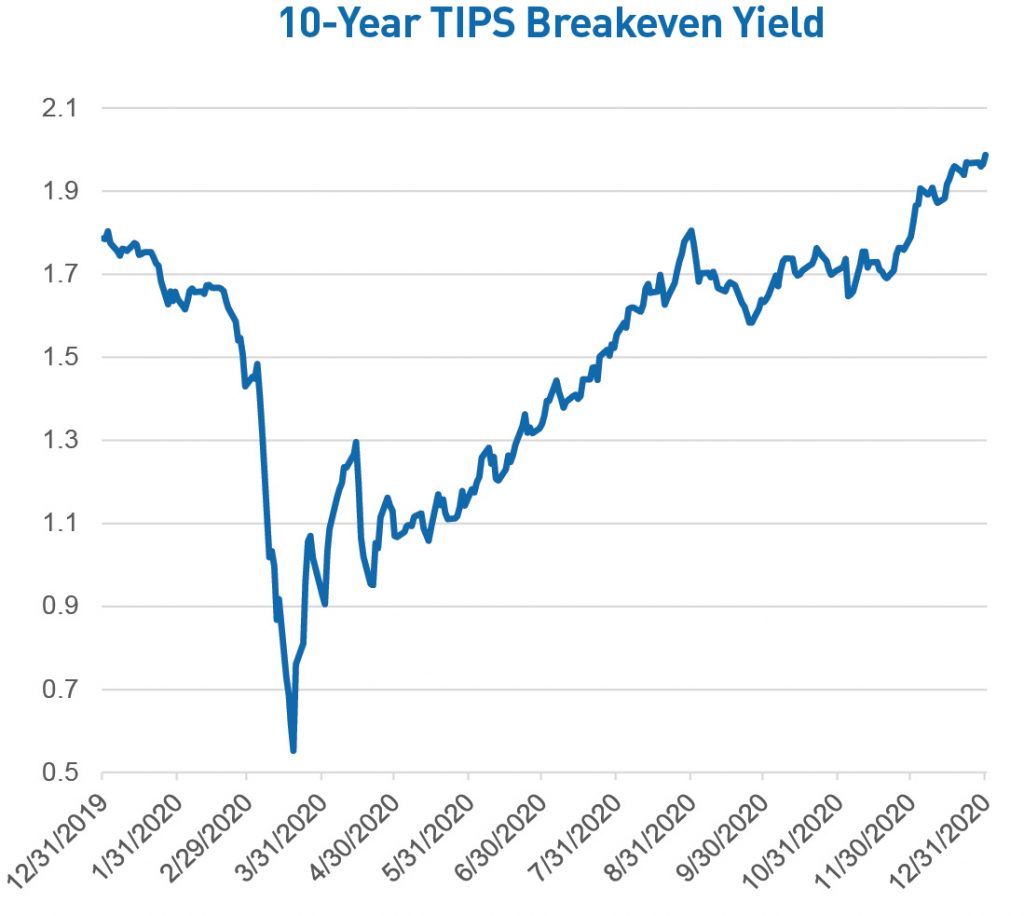

Markets were generally pleased with fiscal developments as another round of stimulus was passed just before year end and a contentious election season ended with Democrats gaining control of the executive branch and, by a narrow margin, both houses of Congress. The UST market has reacted accordingly, building increased reflationary expectations as additional stimulus is expected in 2021. Given the razor thin margins Democrats possess in the House and Senate, bold policy actions seem likely to be constrained. These factors have the potential to improve the growth outlook and increase UST supply, both of which should exert upward pressure on longer term rates.

As of 12/31/2020. Sources: Bloomberg L.P., PNC Capital Advisors

As of 12/31/20. Sources: Bloomberg L.P., PNC Capital Advisors

As of 12/31/20. Sources: Bloomberg L.P., PNC Capital Advisors

Outlook

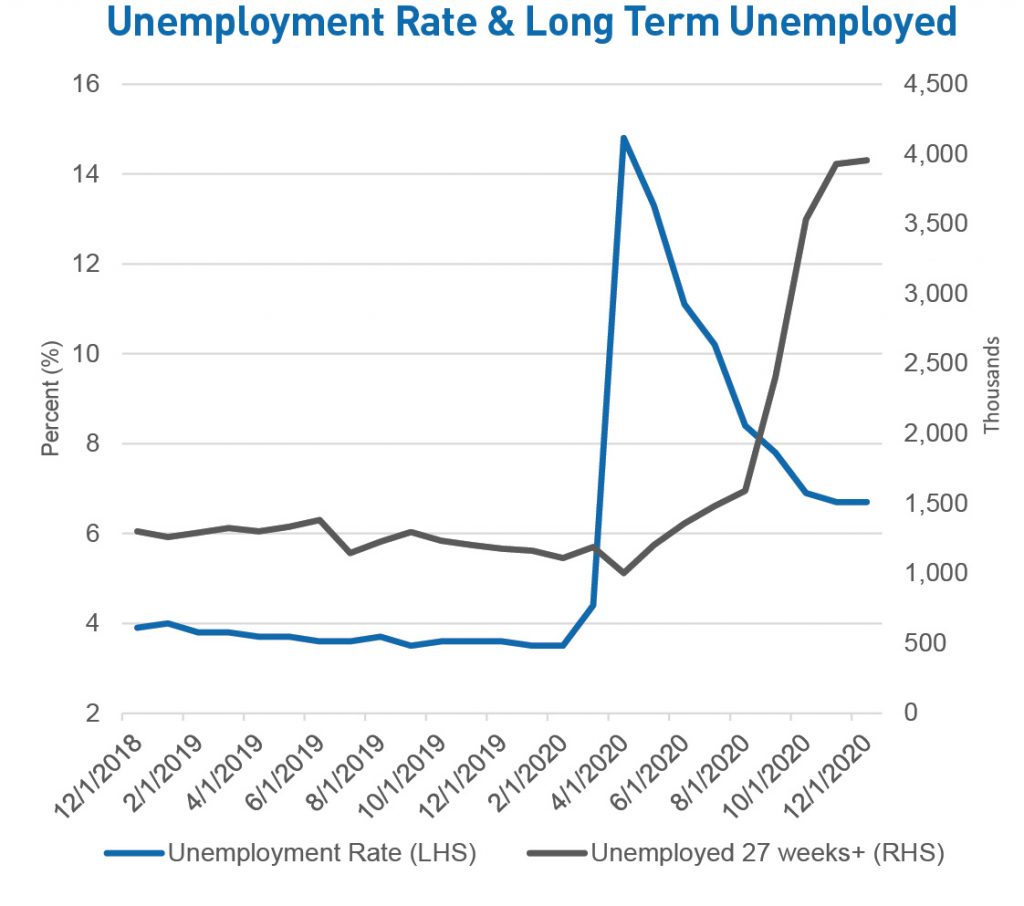

Optimism in financial markets wasn’t restricted solely to governmental policy developments. Of greater importance was rapid progress on effective vaccine development with multiple treatments being deployed by year end. Hope is building that the domestic economy will be able to re-engage in behaviors and activities that have been dramatically impacted by the pandemic. Despite a troubling surge in infection rates, there is confidence that stimulus and pent up consumer demand aided by robust financial and housing markets could offset any near term weakness. Economic trends have been positive in most components of the economy outside of the virus-related sectors that have continued to lag. Labor markets, in particular, have illustrated this disconnect as weakness in leisure and hospitality drags on the employment recovery. Investors have generally embraced positive economic news while dismissing negative news as a pre-cursor for additional stimulus which has led to euphoric market conditions.

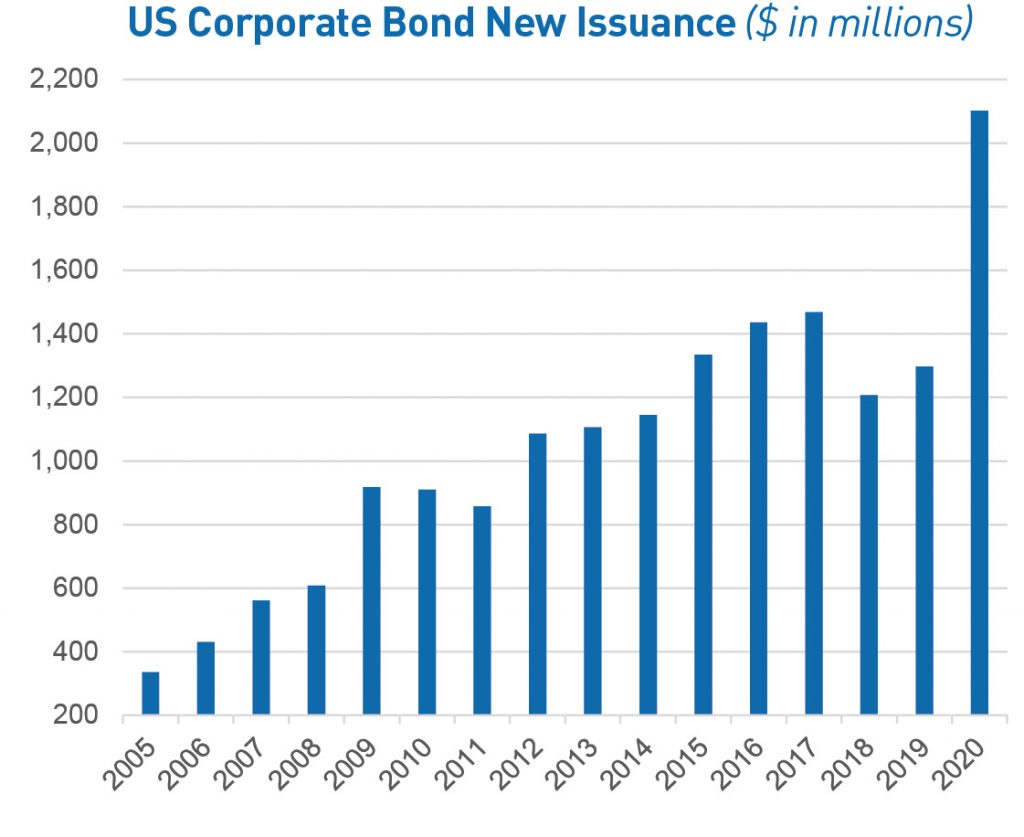

After an impressive rally in the 4Q, credit markets are once again fully valued, similar to where they were in early 2020. For some high quality corporate issuers, spreads are currently at or inside the level at which companies have the ability to call their shorter term debt. We are very mindful of this consideration given the aggressive nature many issuers have taken to term out their maturity profiles given low absolute rates. This has led to a challenging environment for short duration investors as this has both restricted available supply and presented a scenario where certain corporate securities could experience sudden price deterioration should an issuer decide to exercise this call option. Similar challenges exist in longer term corporate securities as well, as the breakeven spread widening that would be needed to overwhelm the annual carry benefit has shrunk to very slim margins. This dynamic is particularly pronounced in higher-quality portions of the market. This was an area of the market we emphasized last year due to issuance patterns resulting from funding dislocations and where we are now actively reducing exposure. We remain generally positive on corporate fundamentals and market technicals and believe subsector allocation and issuer selection will be tantamount to successfully navigating challenging markets in 2021. We expect new issue supply in 2021 to be well off the historic pace of last year, while investor demand will likely continue to remain solid. This should continue to lead to a favorable environment for issuers, with order books significantly over-subscribed for companies looking to bring new debt to market.

As we look to optimize portfolio positioning by emphasizing sectors with favorable risk/return characteristics, we are mindful of both the low interest rate environment and continued elevated levels of uncertainty. Shifts in our allocations to corporate bonds contributed to strong returns over the balance of 2020; as risk premiums have narrowed, we increasingly feel that high-quality structured products (particularly Agency Mortgage-Backed Securities) will provide better return symmetry.

The last two calendar years have been quite favorable for fixed income investors leaving forward return expectations somewhat muted given the current yield environment. However, income and total return are not the sole objectives of our approach. We believe our risk-focused approach provides diversification to a client’s overall portfolio, protecting principal from unforeseen disruptions and maintaining robust liquidity for both anticipated and unexpected cash needs. We achieved successful outcomes for our clients along all of these dimensions not just last year but over longer time periods through a variety of risk and policy regimes. This reflects discipline and adherence to our team-based approach which we believe will continue to deliver consistent excess returns for our clients in the years to come.

Important Disclosures

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

© The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED – NO BANK GUARANTEE – MAY LOSE VALUE