Macro

Throughout April, sticky inflation data and hawkish comments from multiple Federal Reserve (Fed) policymakers confirmed their desire to see further declines in inflation prior to any rate cut decisions. Subsequently, at his May 1 Federal Open Market Committee press conference, Fed Chair Powell delivered mostly dovish remarks, reiterating the Fed’s belief that policy is sufficiently restrictive at current levels, while also acknowledging still-elevated inflation could delay future rate cuts.

Consensus expectations for interest rate cuts, as measured by fed funds futures, decreased during the month to reflect less than two cuts in 2024.

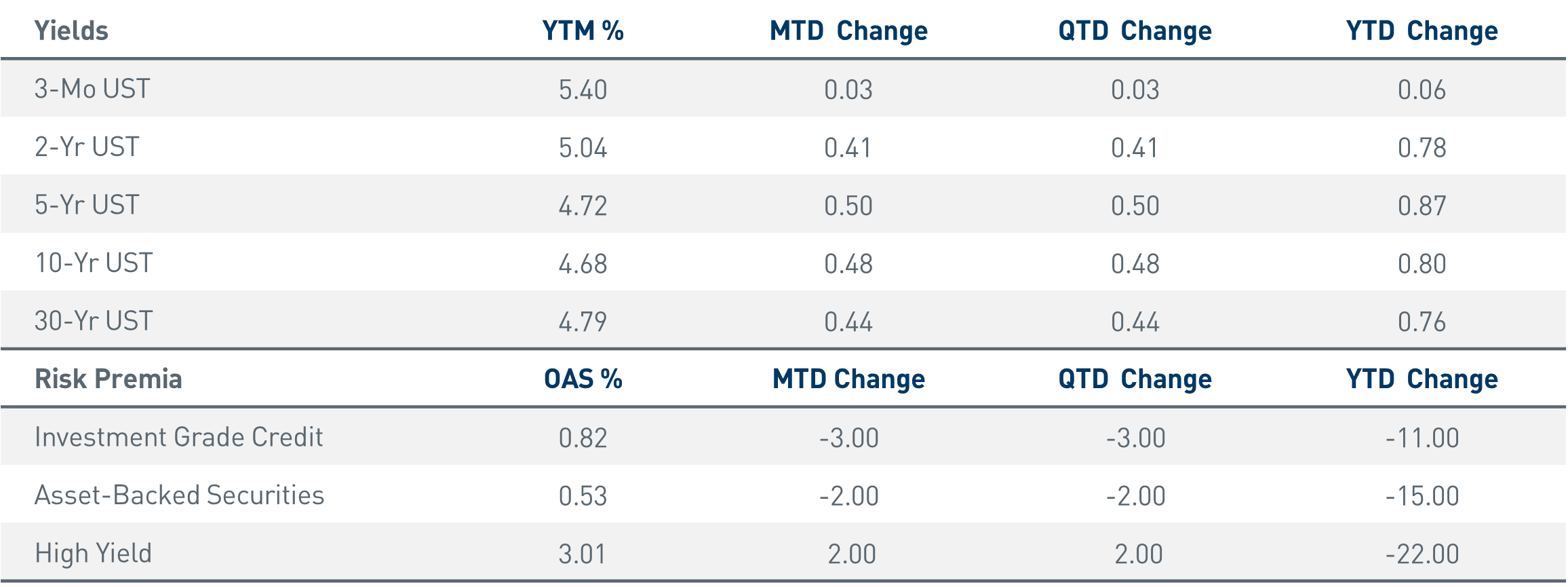

U.S. Treasury yields moved rapidly higher during the month, ultimately reaching their highest levels since November 2023. Correspondingly, interest rate volatility, as measured by the ICE BofAML MOVE Index, increased during the month after hitting a two-year low in March.

Credit

After a record start to the year for issuance, primary markets had their slowest month of the year during April. However, year-to-date issuance of slightly more than $630 billion remains well-ahead of annual issuance at this time last year.

Despite the rise in yields, credit spreads narrowed by 3 basis points (bps) during the month and generated modest, positive excess returns for the sector.

Sub-sector spreads for Industrials and Financials finished the month tighter by 2 bps and 3 bps, respectively.

Structured

Asset-backed security (ABS) issuance remained robust, spreads remained firm and excess returns were modestly positive during the month.

Mortgage-backed securities struggled with the rise in interest rates and ended the month in negative excess return territory after strong March performance.

Chart of the Month: Inflation Measures, YoY

- Inflation remains “sticky,” with some components accelerating in recent months.

- Recent data trends continue to illustrate the need for patience in evaluating the path forward for monetary policy.

As of 4/30/2024. Source: Bloomberg L.P.

Market Data

As of 4/30/2024. Source: Bloomberg L.P.

Bloomberg Sector/Index Performance (USD)

As of 4/30/2024. Source: Bloomberg L.P.

Important Disclosures

This publication is for informational

purposes only. Information contained herein is believed to be accurate, but has

not been verified and cannot be guaranteed. Opinions represented are not

intended as an offer or solicitation with respect to the purchase or sale of

any security and are subject to change without notice. Statements in this

material should not be considered investment advice or a forecast or guarantee

of future results. To the extent specific securities are referenced herein,

they have been selected on an objective basis to illustrate the views expressed

in the commentary. Such references do not include all material information

about such securities, including risks, and are not intended to be

recommendations to take any action with respect to such securities. The

securities identified do not represent all of the securities purchased, sold or

recommended and it should not be assumed that any listed securities were or

will prove to be profitable. Past performance is no guarantee

of future results.

Indices and/or Benchmarks Definitions

PNC Capital Advisors, LLC is a

wholly-owned subsidiary of PNC Bank, National Association, which is a Member

FDIC, and an indirect subsidiary of The PNC Financial Services Group, Inc.

serving institutional clients. PNC Capital Advisors› strategies and the

investment risks and advisory fees associated with each strategy can be found

within Part 2A of the firm's Form ADV.

PNC Capital Advisors, LLC claims

compliance with the Global Investment Performance Standards (GIPS®). A list of

composite descriptions for PNC Capital Advisors, LLC and/or a presentation that

complies with the GIPS® standards are available upon request.

Investments: Not FDIC Insured. No Bank

Guarantee. May Lose Value.

©2024 The PNC Financial Services Group,

Inc. All rights reserved.