Despite the COVID-19 pandemic and its impact on global economies, regulators and financial market participants remain committed to the phase-out of the London Interbank Offered Rate (LIBOR), a globally referenced benchmark for interbank lending.

For more than 30 years, LIBOR has been used by companies and consumers to price countless financial products – from student loans and mortgages to complex derivatives – by acting as the point of reference in variable-rate financial agreements. It is calculated from a daily survey of more than 15 large banks that estimate the cost to borrow from each other on an unsecured basis. Changing industry norms and LIBOR manipulation scandals are driving a shift away from LIBOR, causing interbank lending markets to become much thinner and the number of actual transactions upon which the rate is based to decrease significantly. That has caused regulators globally to actively advocate that markets move away from LIBOR to a more reliable index. In July 2017, the UK’s Financial Conduct Authority (FCA) announced that it will no longer support LIBOR after 2021.

Governments, industry groups, and large financial institutions are all evaluating alternative benchmark rates to LIBOR. While a new benchmark rate has yet to be definitively established, the Alternative Reference Rates Committee (ARRC), convened by the Federal Reserve Board, recommends the Secured Overnight Financing Rate (SOFR) replace US dollar LIBOR. The ARRC also laid out a multi-step plan to further develop SOFR’s usage that includes the creation and publication of rate information, setting up related futures trading, building out swap transactions tied to the new SOFR rate, and establishing SOFR’s indicative term structure.

Unlike LIBOR, the market underlying SOFR is incredibly robust and has broad participation, with about $1 trillion in transactions every day among a diverse set of market participants including asset managers, banks, broker dealers, insurance companies, pension funds, and corporate treasurers.1 This broad participation provides transparency that is designed to protect it from manipulation, and its foundation being the US Treasury repo markets reduces risk of it disappearing.

Despite ARRC’s careful consideration, concerns exist about SOFR as a benchmark rate. Importantly, it will take time for enough liquidity to develop in the SOFR market to validate its reliability and acceptance as a benchmark. Also, SOFR only has a one-day tenor, whereas LIBOR has many different tenors. Without a term structure, there are challenges for both new and existing financial instruments that currently price off LIBOR. SOFR-linked pricing is most comparable to the effective fed funds rate, another overnight rate.

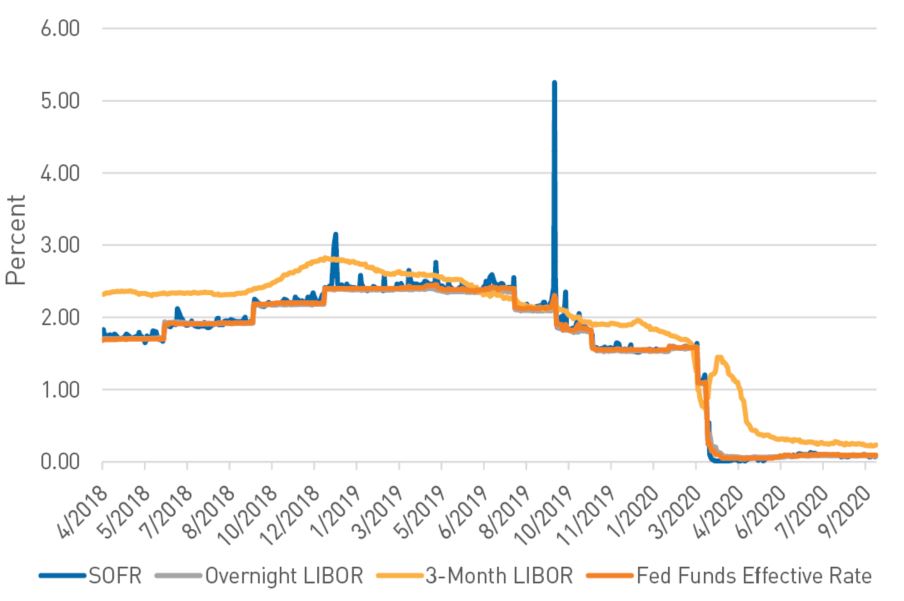

Because SOFR is a spot rate, it is potentially susceptible to large movements from day to day. In fact, it has often spiked at calendar quarter-ends when institutional borrowing tends to increase. In one (extreme) example in mid-September 2019, overnight repurchase agreement (repo) rates spiked, as the confluence of an increase in US Treasury supply, corporate tax day, and a significant decline in bank reserves created an imbalance of available liquidity compared to funding needs. The spike in repo rates caused yields on other overnight securities to rise as well, as issuers needed to entice investors to provide funding away from the repo market. As a result, SOFR also experienced a temporary spike, as it is calculated as an average of repo trades from the previous day. SOFR rose more than 300 basis points on September 17, reaching a high of 5.25% before returning to a more normalized level within two days. The Federal Reserve (Fed) responded quickly with a series of open market repo operations that eased the stresses in the money markets. In fact, as soon as the operations were announced, yields snapped back. As banks utilized the available repo for funding, yields dropped further due to more than ample liquidity.

Figure 1.

Comparable Short-Term Benchmarks

As of 9/30/2020. Source: FactSet

Reassuringly, amid the COVID-induced market volatility during spring 2020, SOFR appeared resilient. SOFR, along with other overnight funding rates, moved in concert with the rates set by the Fed, faring well despite the period of extreme financial market stress.

It has been estimated that US dollar LIBOR is linked to over $200 trillion of financial products.2 While consensus has yet to definitively settle on a single LIBOR substitute, market participants must begin adjusting to its discontinuation, as the implications are far-reaching. For example, existing bond indentures for LIBOR-linked securities maturing beyond 2021 will need to be revised to reference a new benchmark (or a mechanism for a new benchmark to be selected). Additionally, the indenture language for newly issued bonds that mature beyond 2021 must be flexible enough to accommodate whichever benchmark is chosen to supersede LIBOR. No small task indeed!

So far, SOFR appears to be LIBOR’s heir presumptive, as there has been an increase in the use of SOFR as a benchmark for floating-rate debt. In the cash bond market, Fannie Mae, the World Bank, and Credit Suisse were among the first to issue floating-rate notes (FRNs) based on SOFR. J.P. Morgan was the first money-center bank to issue a fixed-to-floating-rate preferred security that references SOFR. In the loan market, Fannie Mae and Freddie Mac have announced plans to develop new adjustable-rate mortgage products that would rely on SOFR instead of LIBOR. Currently, government-sponsored enterprises (GSEs) make up an overwhelming portion of SOFR-linked debt, accounting for roughly 75% of all SOFR FRN debt issuance.3

The transition to SOFR temporarily appeared in jeopardy, as market disruptions from the onset of COVID-19 and resulting wide-ranging economic lockdowns and work-from-home orders put planning meetings on hold for more than a month, but they have since resumed in earnest. The global timeline to move to away from LIBOR remains on track, and the FCA has reaffirmed that “the central assumption that firms cannot rely on LIBOR being published after the end of 2021 has not changed.”4

While the initial rollout of SOFR has encountered several challenges, we continue to work to understand the implications of this change and have been active buyers of SOFR-linked agency debt since October 2018. These securities have and continue to provide a yield advantage over fixed-rate bonds with comparable maturities, as well as LIBOR-linked floating-rate debt. Additionally, agency SOFR FRNs have helped us avoid some of the uncertainty surrounding the LIBOR phase out, and the one-day resets have enabled us to enhance yield while managing the weighted average maturity of our clients’ portfolios. We expect the many challenges facing SOFR will be addressed in the months ahead, including potential tax, accounting, and regulatory hurdles. Accordingly, we will continue to closely monitor the transition to a new reference rate and take appropriate action in client portfolios as necessary.

- New York Fed Speech, Nathaniel Wuerffel, “Transitioning Away From LIBOR: Understanding SOFR’s Strengths and Considering the Path Forward,” September 18, 2020

- ARRC, “SOFR Summer Series: SOFR Explained,” 15 July 2020, accessed through the ARRC website.

- Bloomberg L.P., PNC Capital Advisors

- FCA, “Impact of the coronavirus on firms’ LIBOR transition plans,” 25 March 2020, accessed through the FCA website.

Important Disclosures

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

©2020 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE