First Quarter Highlights

- At its March 18 meeting, the Federal Open Market Committee (FOMC) held rates steady, maintaining the target range for the federal funds rate at 3.50% - 3.75%. The post-meeting statement emphasized the Committee's ongoing consideration of risks related to both maximum employment and price stability.

- President Trump announced Kevin Warsh as his nominee to serve as the next chair of the Federal Reserve (Fed), with current Chair Jerome Powell's term concluding in May.

- The broadening geopolitical conflict with Iran has become the primary driver of market volatility, and the path to a sustainable resolution remains uncertain as of this writing.

- Surging energy prices are expected to significantly impact headline inflation; there are heightened concerns that a lengthy conflict in the Middle East could impact core inflation and the growth outlook.

- While credit fundamentals continue to be favorable, risk premia in sectors considered more susceptible to the effects of artificial intelligence (AI) face increased pressure.

- While investor concern regarding the stability of private credit markets continues to rise, the effects on public investment-grade markets appear limited thus far. Despite increased caution, there continues to be strong demand for investment grade credit — as evidenced by the record more than $635 billion in new issuance during the quarter.

- Credit spreads moved higher during the quarter, which resulted in negative excess returns for the sector. Structured products proved to be more defensive, yielding modestly positive excess returns.

Duration Positioning

Neutral

Remain neutral on duration positioning given balanced yield and return symmetry.

Credit Sector

Shifting from underweight towards neutral

Improved valuations offered opportunities for strategies to increase allocations. Within sub-sectors, strategies are overweight banking and energy, while underweight capital goods, insurance and non-corporate credit.

Structured Products

Overweight

Allocations in asset-backed securities (ABS) have been moderated across strategies but remain overweight relative to benchmarks. Allocations in MBS remain overweight within both aggregate and non-aggregate styles.

First Quarter Market Summary

During the first quarter, fixed income markets encountered many obstacles, including concerns about AI-driven disruptions, increased strain in private credit markets and escalating geopolitical tensions in the Middle East. Global bond yields rose as higher energy prices contributed to increased inflation expectations and challenged investor risk tolerance amid the onslaught of new uncertainties. Although market conditions remained volatile, corporations seeking to raise capital were able to access investment grade markets effectively, resulting in gross issuance that exceeded $635 billion—a record amount for first-quarter new issuance.

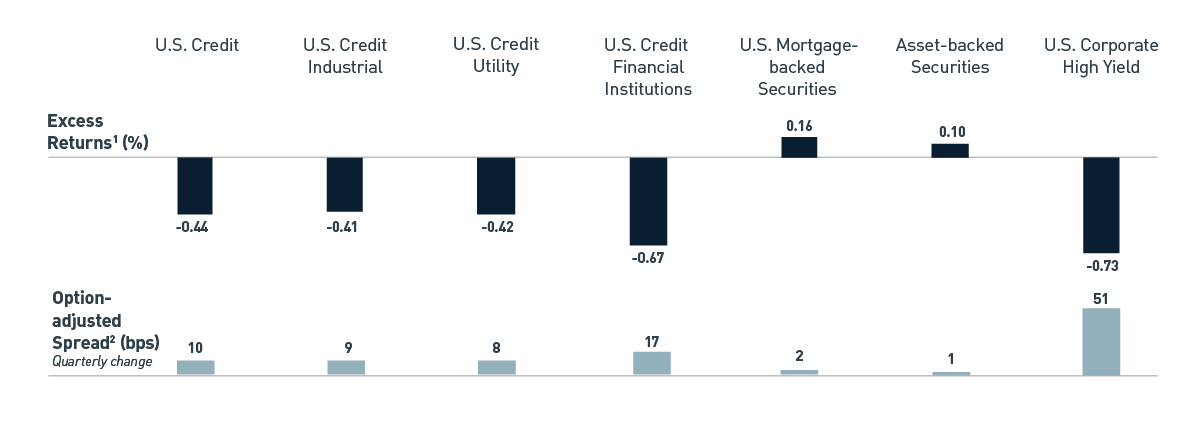

After strong performance during January and February, the Bloomberg US Aggregate Bond Index came under pressure in March as the yield-to-worst increased 41 basis points (bps) to 4.57% during the month. Shorter-dated U.S. Treasury (UST) yields rose more significantly as market expectations for Fed policy easing cooled, resulting in a flatter, overall yield curve. This resulted in a first-quarter total return of -.05% for the index. Investment grade credit spreads increased 10 bps, leaving the Bloomberg US Credit Index option-adjusted spread (OAS) at 83 bps, and resulting in 44 bps of negative excess return. Securitized sectors proved more defensive, the MBS and ABS sectors generated positive excess returns of 16 bps and 10 bps, respectively (Figure 1).

Figure 1. First-quarter Sector Excess Returns and Option-adjusted Spreads of Bloomberg U.S. Aggregate and U.S. Corporate High Yield Indices

As of 3/31/2026. Source: Bloomberg L.P. View accessible version of chart.

1 Excess total return of each index/component of the index relative to the duration-matched UST Index.

2 Of the Bloomberg U.S. Aggregate Bond Index.

War & Worries Draw Attention Away from the Fed

The FOMC held the fed funds rate steady during the first quarter, after three consecutive 25-bp cuts in late 2025. Given Fed commentary regarding inflation and employment in the weeks leading up to the meeting, markets had largely expected a continued pause in policy rate adjustments.

However, more recent inflation data has presented a mixed picture. Both headline and core (inflation excluding the more volatile food and energy categories) U.S. Consumer Price Index data have declined, whereas the Fed's preferred inflation gauge, the Personal Consumption Expenditures (PCE) index, is proving more stubborn. For the first time in almost two years, the year-over-year change in core PCE data has exceeded 3%, which suggests that pricing pressures persist.

The latest labor market data has also been inconsistent; the Bureau of Labor Statistics' February employment report was weaker than anticipated, but it was followed by a much stronger March result. The unemployment rate remains low, at 4.3%, but it has been partially influenced by a declining labor force participation rate, which has steadily declined over the last few months.

Other measures of job market health remain soft, particularly outside of the healthcare sector, which is where most of the labor gains have been concentrated throughout the past year. Following the significant job growth deceleration that occurred in 2025, the three-month moving average of approximately 70,000 jobs added in the first quarter of 2026 firmed from late last year and supports a relatively stable unemployment rate given demographic and immigration trends.

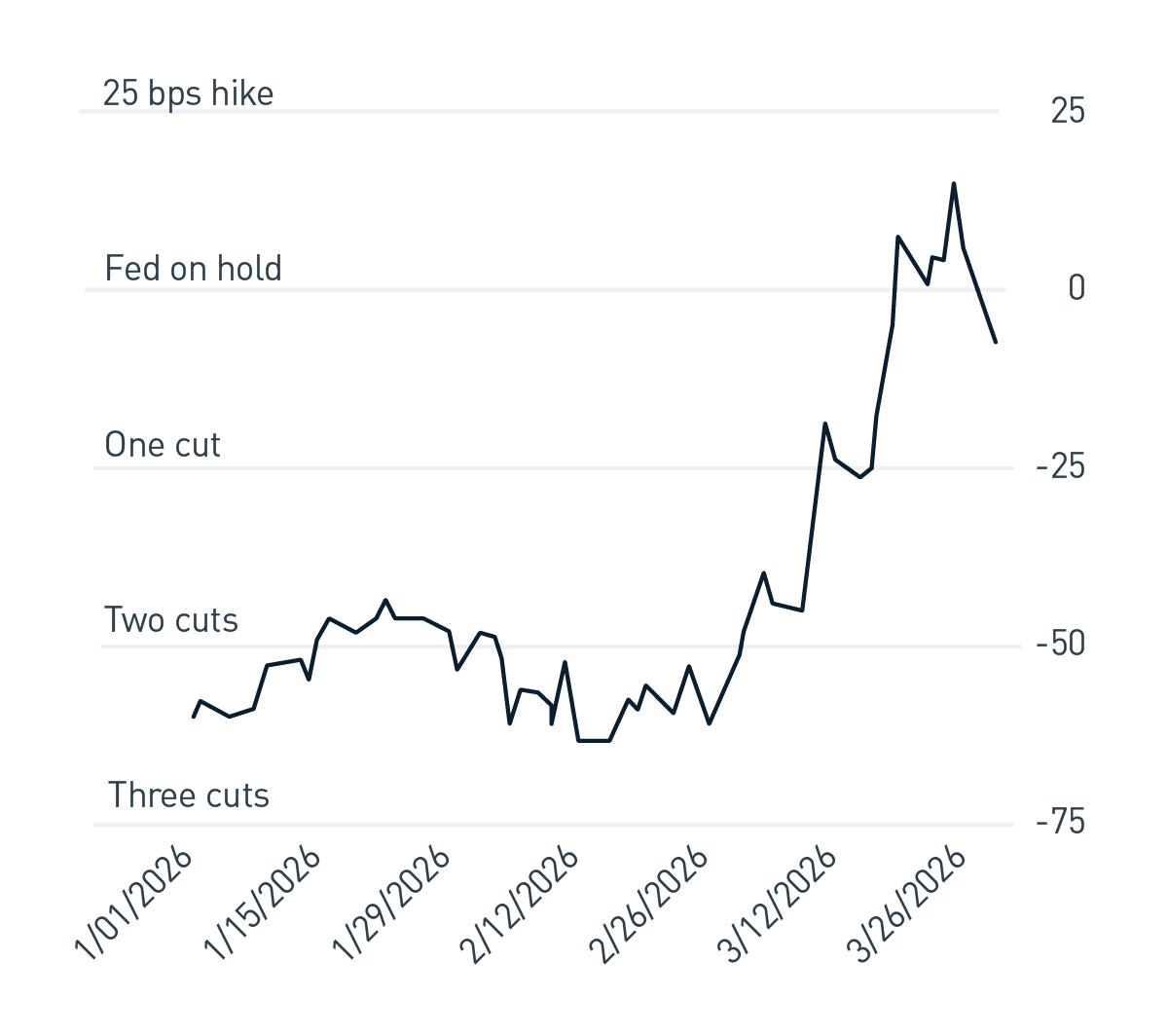

Economic data, however, have largely taken a back seat in investor minds since the beginning of the Iran conflict as upcoming inflation data is expected to be significantly impacted by surging energy prices. UST yields have risen considerably since the conflict began, especially for shorter-dated maturities as expectations for the future path of policy rates shifted dramatically (Figure 2).

Figure 2. Amount of Fed Cuts Priced by December 2026

As of 3/31/2026. Source: Bloomberg L.P. View accessible version of chart.

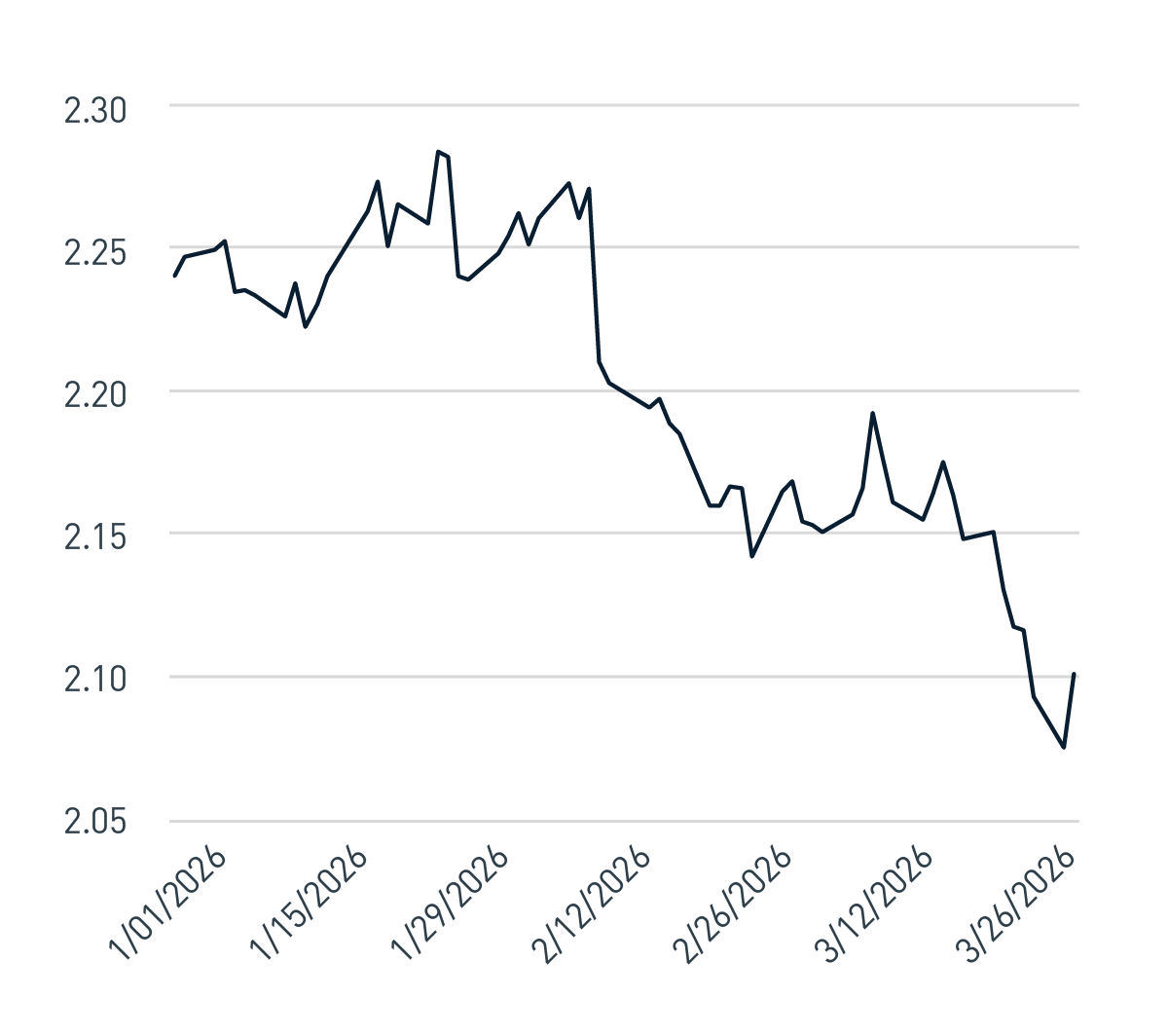

The degree to which increased oil prices will affect core inflation is still uncertain, and this issue will be a primary consideration for the Fed. Chair Powell recently stated that the Fed would likely look past elevated oil prices in the near term as energy shocks have historically subsided quickly, and instead, remain focused on forward-looking inflation expectations, which remain reasonably well-anchored (Figure 3). Additionally, the prospect of a prolonged conflict resulting in a persistent energy shock would likely weigh on growth and potentially employment, perhaps warranting a more dovish stance from the FOMC.

Figure 3. 5-year Forward Breakeven Inflation Rate

As of 3/31/2026. Source: Bloomberg L.P. View accessible version of chart.

President Trump formally nominated Kevin Warsh to serve as the next chair of the Fed once Chair Powell's term ends in May. The timing of Warsh's confirmation is uncertain however, as key Republican senators oppose moving forward with Warsh's nomination until the Justice Department's investigations into Chair Powell are completed. At the March FOMC meeting, Chair Powell indicated that he would continue to serve as chair until his successor is confirmed. He also stated that he would be willing to continue to serve on the Fed Board of Governors following the appointment of the next chair, contingent upon what would best serve the interests of the Fed.

Portfolio Positioning — AI-nxiety and War Fog Present Opportunities

Prior to the Iran conflict that began on February 28, credit markets were already contending with concerns about AI-driven disruptions and worsening investor sentiment in the private credit market. While the broader economic and workforce implications resulting from widespread AI adoption are challenging to assess, investors have recently demonstrated increased caution regarding specific industries perceived as vulnerable to market share loss.

In particular, software companies came under pressure during the first quarter as AI innovators unveiled tools with the potential to infringe on existing applications. Credit spreads for the companies seen as most vulnerable, widened as investors re-evaluated select exposures. Broader concerns related to deteriorating credit quality and the private credit sector's rapid growth are amplifying anxiety in private credit, resulting in substantial redemption requests in certain funds and, in turn, driving driving a negative feedback loop as managers institute caps on flows given the asset class's inherent illiquidity.

Large financial institutions appear to be adequately insulated to private credit, but should delinquencies continue to increase, investors would likely become more cautious. Similarly, impacts within the broader public investment grade and high yield markets remain limited. We believe the proliferation of private credit vehicles contributed to a broader trend of risk spread compression, and that it has the potential to impact public markets as liquidity is withdrawn and risk appetites become more discerning.

Despite the various headwinds that weighed on risk sentiment during the first quarter, investment grade companies were aggressive issuers of new debt and placed more than $630 billion during the quarter. This was partially aided by the continued, super-sized issuance from the large technology “hyperscalers” seeking to finance robust capital expenditures in AI-related infrastructure. Investors were eager buyers as evidenced by the historic $129 billion order book for Oracle Corp.'s $25 billion deal in February, and then nearly equaled by Amazon.com Inc.'s $126 billion order book for their $37 billion bond sale in March.

Recent issuance patterns contributed to a modest widening of credit spreads; the Bloomberg US Credit Index rose from a historically low 67 bps in late January, to a high of 86 bps by mid-March. Throughout the quarter, we leveraged opportunities across both new issues and cheapened secondary offerings to add exposure across strategies as valuations became more compelling. Our confidence in adding credit in the face of macro uncertainty was aided by the fact that we entered the quarter with underweight allocations in credit due to the expensive level of valuations. The quarter's episodic volatility and cheapened valuations, however, led us to shift positioning in most of our strategies to a more neutral allocation in credit.

The resurgence of interest rate volatility during March created opportunities within the agency MBS sector as well with wider current coupon spreads. Fundamentals for agency MBS are solid, with modest prepayments and moderating rate volatility so far in April. Meanwhile, demand is supported by the increased involvement from Fannie Mae and Freddie Mac, given their $200 billion purchase commitment. We have maintained overweight allocations to agency MBS across our strategies as valuations remain attractive relative to credit, and benefit from a lower volatility profile (Figure 4).

Figure 4. Trailing 12-month Excess Return Volatility in the Bloomberg U.S. Credit vs. Bloomberg U.S. MBS Index

As of 3/31/2026. Source: Bloomberg L.P. View accessible version of chart.

Outlook — Dire Straits

Markets are on tenterhooks as the Iran conflict continues and a near-term agreement for a lasting ceasefire remains elusive. Energy prices are significantly higher than before the conflict began and seem unlikely to fully retrace, keeping upward pressure on headline inflation and impacting marginal consumer spending as we head into the summer travel season.

While financial conditions have tightened modestly, we are not seeing signs of acute stress as moderating volatility brings credit spreads back towards recent lows. As first-quarter earnings season kicks off, we will be attuned to management commentary on corporate outlooks for the remainder of 2026.

With the labor market in a delicate state of balance and concerns about inflationary pressures resuming, we expect the Fed to remain cautious in adjusting policy. At the same time, the ongoing costs of the conflict will put additional stress on an already challenged fiscal budget and likely keep UST rates elevated.

We believe the return symmetry within fixed income remains reasonably attractive; the Bloomberg US Aggregate Index is yielding approximately 4.5% as of this writing, which should help to cushion portfolios against the risk of a further increase in interest rates. Given heightened uncertainty in the global macro outlook and domestic policy headwinds, we maintain a more defensive portfolio risk posture with emphasis on short-duration credit and high-quality agency MBS.

Figure 1. Fourth-quarter Sector Excess Returns and Option-adjusted Spreads

| Category |

Excess Returns Quarter (%) |

Option-adjusted Spread, Quarterly Change (bps) |

| U.S. Credit |

-0.44 |

10 |

| U.S. Credit Industrial |

-0.41 |

9 |

| U.S. Credit Utility |

-0.42 |

8 |

| U.S. Credit Financial Inst. |

-0.67 |

17 |

| MBS |

0.16 |

2 |

| ABS |

0.10 |

1 |

| U.S. Corporate High Yield |

-0.73 |

51 |

Figure 2. Amount of Fed Cuts Priced by December 2026

| Date |

Cuts |

| 1/1/2026 |

-59.7 |

| 1/15/2026 |

-48.2 |

| 1/29/2026 |

-48 |

| 2/12/2026 |

-58.9 |

| 2/26/2026 |

-56.8 |

| 3/12/2026 |

-18.9 |

| 3/26/2026 |

14.4 |

Figure 3. 5-year Forward Breakeven Inflation Rate

| Date |

Rate |

| 1/01/2026 |

2.24 |

| 1/15/2026 |

2.23 |

| 1/29/2026 |

2.24 |

| 2/12/2026 |

2.21 |

| 2/26/2026 |

2.16 |

| 3/12/2026 |

2.17 |

| 3/26/2026 |

2.11 |

Figure 4. Trailing 12-month Excess Return Volatility in the Bloomberg U.S. Credit vs. Bloomberg U.S. MBS Index

| Date |

U.S. Credit Trailing 12-mo Volume |

U.S. Mortgage-backed Securities Trailing 12-mo vol. |

| 12/31/2024 |

.084 |

0.47 |

| 2/28/2025 |

0.81 |

0.43 |

| 4/30/2025 |

0.65 |

0.41 |

| 6/30/2025 |

0.64 |

0.44 |

| 8/29/2025 |

0.66 |

0.39 |

| 10/31/2025 |

0.89 |

0.56 |

| 12/31/2025 |

0.88 |

0.70 |

| 2/27/2026 |

0.87 |

0.37 |

Important Disclosures

Index definitions are available at https://www.pnccapitaladvisors.com/index-definitions/

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

©2026 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE