“Price is what you pay, value is what you get.” – Warren Buffett

Credit spreads keep on tightening to some of the richest levels we’ve observed over 25-plus years of index data from Bloomberg and the Intercontinental Exchange (ICE) — and we’re looking elsewhere for relative value.

October was supposed to herald falling leaves and falling interest rates in the wake of the Federal Reserve’s (Fed’s) September pivot. Instead, the U.S. Treasury (UST) market responded to a healthy September payrolls report and resilient consumer spending by moderating implied expectations for rate cuts through the balance of 2024 and into 2025, leading yields higher. Corporate Credit (Credit) spreads reacted favorably to higher yields and solid economic fundamentals by narrowing to historically tight levels. As a key tenet of our risk-focused investment approach is an emphasis on the symmetry of expected return — that is, the balance between downside risk and the compensation for that risk in the form of return — we currently see more attractive relative value opportunities in Structured Products.

It’s All Aces in Credit

Any way you cut it, Credit looks expensive. One lens through which we evaluate risk sectors and their relative value is by performing a breakeven analysis — that is, for a given cohort of securities, what is the level of spread-widening over a specified period that would offset the carry associated with the starting spread? Spread duration informs this analysis, as extending maturities often amplifies volatility and thereby reduces the benefits from incremental carry.

When we examine the current Credit environment through this lens, the results are stark. As of October 16, the six-month breakeven spread on Credit was a mere 6 basis points (bps) and ranked in the fifth percentile of most expensive values dating back to 1997 (Figures 1, 2).

Figure 1. Six-month Breakeven Spread, ICE BofA U.S. Corporate & Yankees Index (bps)

| 6 |

1-3 Yr |

3-5 Yr |

5-7 Yr |

7-10 Yr |

10+ Yr |

| AAA-AA |

6 |

6 |

4 |

4 |

2 |

| A |

12 |

8 |

7 |

6 |

3 |

| BBB |

20 |

13 |

10 |

9 |

5 |

As of 10/16/24. Source: ICE BofA Indices

Figure 2. Percentile Rank, Six-month Breakeven Spread, ICE BofA U.S. Corporate & Yankees Index

| 5 |

1-3 Yr |

3-5 Yr |

5-7 Yr |

7-10 Yr |

10+ Yr |

| AAA-AA |

4 |

13 |

3 |

9 |

1 |

| A |

13 |

11 |

7 |

14 |

0 |

| BBB |

13 |

9 |

5 |

9 |

2 |

For the period 12/31/97 - 10/16/24. Source: ICE BofA Indices

To further contextualize current breakeven spread levels, we also look at spread volatility. Figure 3 depicts the semi-annualized volatility of monthly changes in the option-adjusted spread (OAS) of corporate credit indices since September of 2020. We believe comparing these volatility measures to breakeven spreads illustrates the poor current value proposition and imbalanced return symmetry of Credit. For example, the OAS for the BBB-rated cohort of the ICE BofA 5-7-year U.S. Corporate Index had a standard deviation of 33 bps, roughly three times the current six-month breakeven spread of 10 bps.

Figure 3. Semi-annualized Volatility of Monthly Change

in OAS, ICE BofA U.S. Corporate & Yankees Index (bps)

| 23 |

1-3 Yr |

3-5 Yr |

5-7 Yr |

7-10 Yr |

10+ Yr |

| AAA-AA |

13 |

15 |

17 |

20 |

20 |

| A |

23 |

26 |

25 |

26 |

23 |

| BBB |

35 |

34 |

33 |

33 |

30 |

For the period 9/30/20 - 9/30/24. Source: ICE BofA Indices

As valuations further ascend into rarified air, we have continued to actively prune Credit risk (for more information, please read our 3Q24 Quarterly Market Commentary) and moved to an underweight position in our Broad Market strategies. We consider the current symmetry of return to be relatively poor across most of the Credit sector. While the market seems caught up in a Goldilocks daydream, we’ll hang up our overweight and see what tomorrow brings.

Credit vs. Structured Products: A Tale of Two Risk Sectors

In contrast with the Credit sector, we continue to find attractive relative value opportunities in Structured Products, across both asset-backed and agency mortgage-backed securities (ABS and MBS, respectively).

In ABS, our sole focus remains AAA-rated structures supported by robust credit enhancements. Valuations are attractive relative to lower-rated Industrial corporate bonds and, given the dearth of AAA-rated supply in other sectors, we believe ABS allocations remain a favorable way to enhance yield as we wait for better entry points in riskier alternatives.

MBS, based on our analysis, also remains attractive versus Credit; however, agency MBS has delivered uneven excess returns during the Fed’s most recent tightening campaign. We ascribe this performance to three primary market dynamics: interest rate volatility, the overall level of rates and the slope of the UST curve. Since these three factors are highly correlated, their impacts on risk premiums in MBS are interrelated.

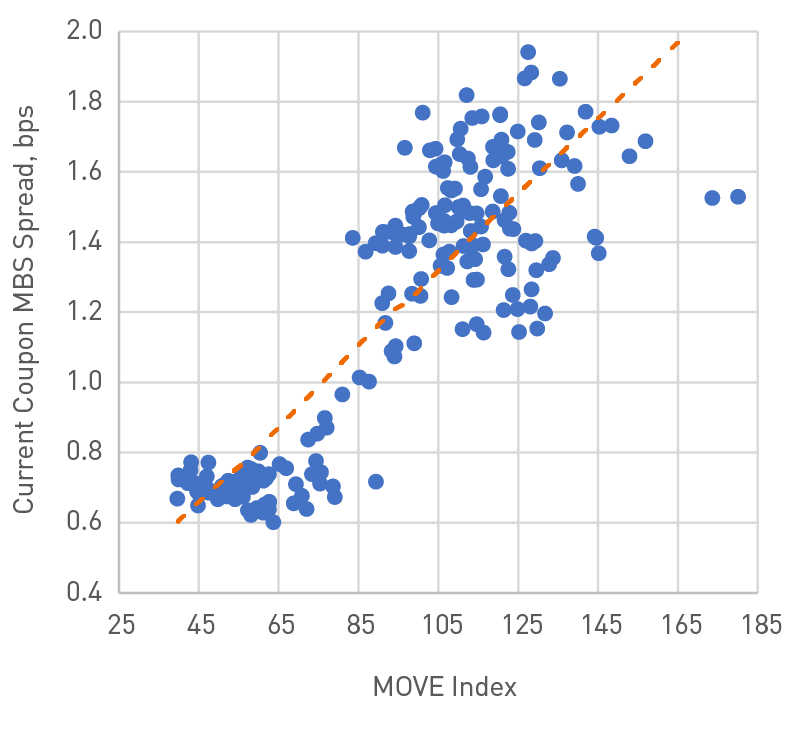

Interest rate volatility: For MBS generally, the value of prepayment options for the mortgage holder increases as rate volatility increases. The inverse is true for the bondholder; as rate volatility increases, the risk premium in MBS increases to compensate for more cash flow uncertainty. A persistent theme throughout the Fed’s tightening regime was elevated interest rate volatility, which periodically spiked as markets shifted in anticipation of policy changes. Elevated volatility was further amplified during October as the 2024 U.S. election loomed and improving economic fundamentals instilled doubt about the continued pace of the Fed’s easing cycle (Figure 4). This move caused MBS to give back all the outperformance the sector accrued over the previous two months.

Figure 4. ICE BofAML MOVE Index vs. Current

Coupon MBS Spread

For the period 9/30/20 - 9/30/24. Source: Bloomberg L.P.

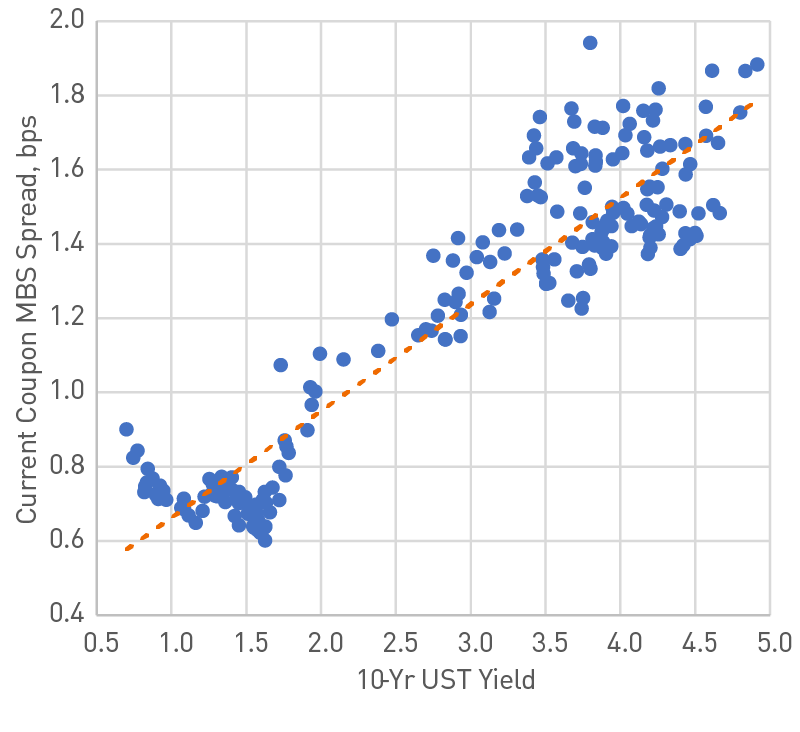

The level of interest rates: The risk premium in MBS (or current coupon spread) tends to exhibit a positive correlation to the overall level of interest rates (Figure 5). Over the last four years, as UST yields rose, MBS current coupon spreads widened; when yields fell, spreads compressed. We ascribe the positive relationship between yield levels and MBS spreads to the higher rate-volatility regime discussed above and the impacts of convexity hedging. We would posit that during periods of meaningful shifts in the overall yield environment, investors have exhibited patience when adjusting MBS allocations, leading to outsized spread changes.

Figure 5. 10-Yr UST Yield vs. Current Coupon MBS Spread

For the period 9/30/20 - 9/30/24. Source: Bloomberg L.P.

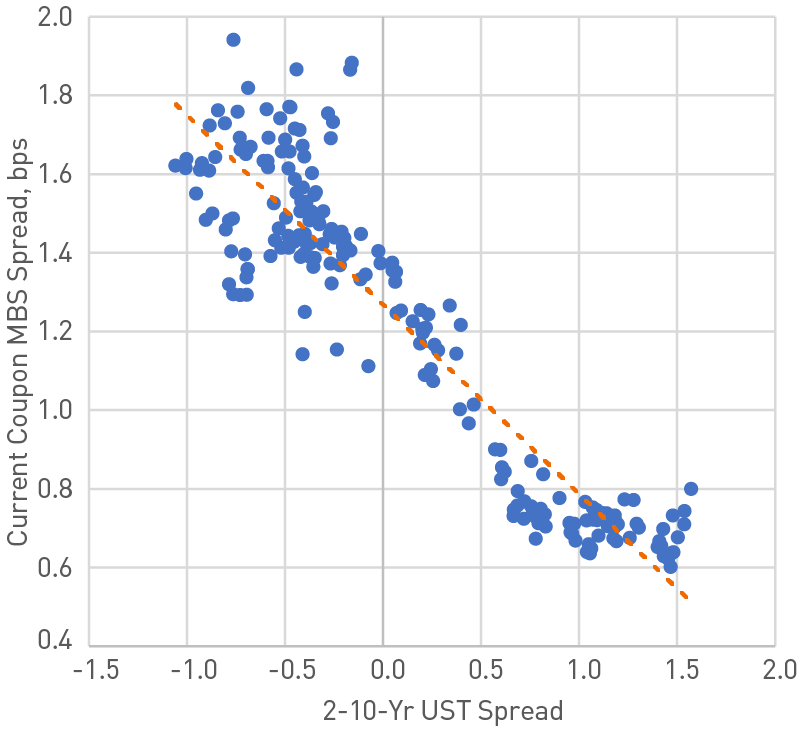

The slope of the UST curve: Shortly after the Fed began its tightening campaign, the slope of the 2-10-year UST curve shifted from positive to negative. This inversion reached almost 110 bps in mid-2023 and presented a headwind to MBS performance. As shown in Figure 6, the current coupon spread of agency MBS has exhibited a negative correlation to the UST curve’s slope, allowing the sector to remain attractive even as the Fed has begun easing policy. We believe the negative correlation between MBS spreads and the UST curve is partly driven by the use of short-term rates to fund carry trades in MBS. Inverted curves make carry trades less profitable; therefore, a steeper UST curve may increase investor demand for the MBS sector.

Figure 6. 2-10-Yr UST Spread vs. Current Coupon MBS Spread

For the period 9/30/20 - 9/30/24. Source: Bloomberg L.P.

Playing the Mean Reversion Card in Agency Mortgages

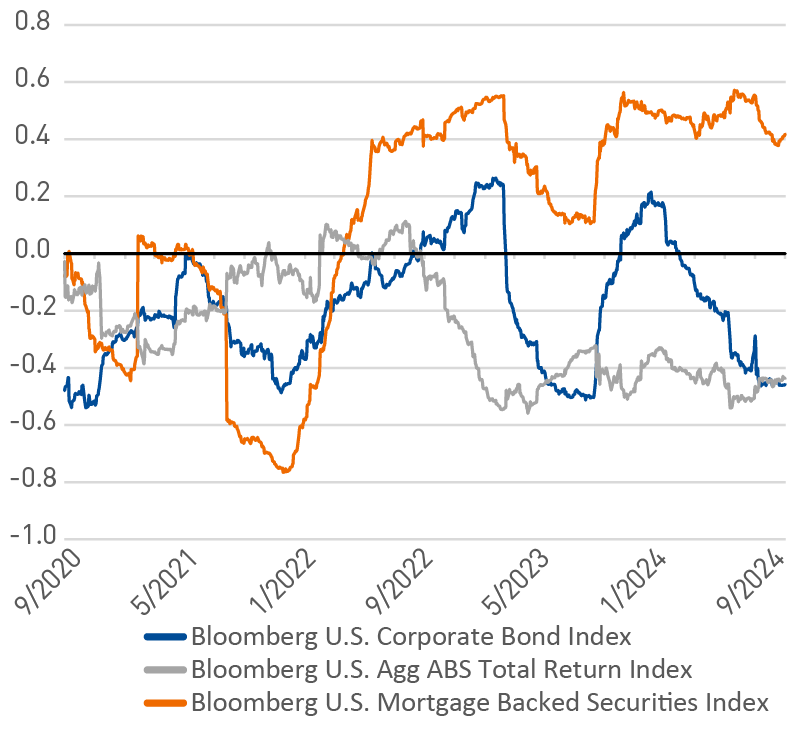

During 2024, the excess return profiles of Credit and agency MBS have meaningfully diverged. As shown in Figure 7, agency MBS performance has suffered as it has exhibited a positive correlation to broad movement in UST yields. As we discussed, there are other factors influencing this correlation, including the slope of the UST curve and the overall level of volatility. In stark contrast, Credit performance has benefited from higher yields and shown an increasingly negative correlation with USTs over the course of 2024.

Figure 7. Rolling Six-month Correlation of Excess Returns and Bloomberg U.S. Treasury Index

As of 9/30/24. Source: Bloomberg L.P.

When looking at agency MBS through our risk framework, valuations are compelling with percentile ranks considerably higher than all Credit cohorts. The sector’s fundamental outlook is good as prepayments remain low and much of the mortgage universe remains significantly “out of the money,” with the average outstanding mortgage rate approximating 4%.

While factors such as a historically large current account deficit and the trillion-dollar annual federal interest expense may influence the UST term premium, we believe interest rate volatility and the overall level of yields have experienced their cycle peaks. Additionally, although core inflation remains above the Fed’s 2% target, in our view, inflation has also peaked. The Fed has communicated its intent to normalize policy over time, which should enable the UST curve to disinvert.

The initial market reaction to the U.S. election is discounting expectations for lower taxes, better growth and higher inflation. Ultimately, we believe economic fundamentals and the path of Fed policy will be the primary drivers of rate volatility over the near term. We believe agency MBS offers equivalent yield and better spread opportunities to Credit broadly, and we plan to lean into a contrarian play as this relative value opportunity has become more pronounced.

Important Disclosures

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). Bloomberg or Bloomberg’s licensors own all proprietary rights in the Bloomberg Indices. Bloomberg does not approve or endorse this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection there with.

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

Indices and/or Benchmarks Definitions

©2024 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE