Macro

The July 30 Federal Open Market Committee meeting was largely uneventful as there were no adjustments to the policy rate or material changes to the prior meeting’s statement.

While it was notable that two members of the Federal Reserve Board of Governors dissented, preferring a rate cut at the meeting, this was generally anticipated in advance.

July inflation reports showed upward price pressures on goods, possibly indicating passthrough impacts from tariffs.

Labor reports for July were disappointing, with a cumulative 258,000 negative revision to the prior two months of payroll growth. The unemployment rate rose to 4.2%, while the labor force participation rate fell to 62.2%.

Following the lackluster report, implied market probabilities for a September rate cut increased to nearly 90%.

Credit

During July, approximately $80 billion in new issuance was priced, slightly below expectations. Forecasts for August anticipate $95 billion of new supply.

In July, credit markets experienced strong performance as the Bloomberg U.S. Investment Grade Credit Index tightened seven basis points (bps), to an option-adjusted spread of 72 bps.

This represented a new year-to-date low and was within just one basis point of the post-global financial crisis low of 71 bps that was reached in November 2024.

Structured

July activity in ABS markets was robust with $41.1 billion in new issuance.

Strong technical demand remains entrenched as deals remain well oversubscribed, leading to tighter spreads.

Excess returns for the Bloomberg Mortgage-backed Securities Index were flat for the month as lower quality sectors outperformed.

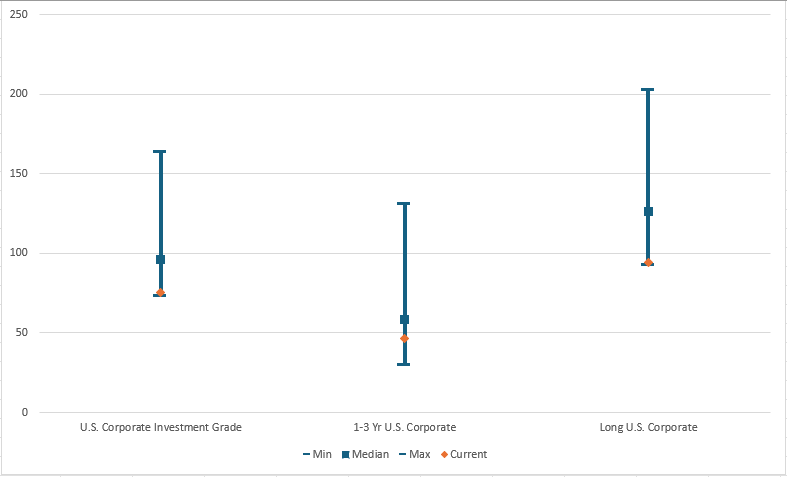

Chart of the Month

Corporate Bond Spreads, 12/31/21-Present*

- Investment-grade risk premiums are currently expensive relative to historical ranges.

- Long-duration spreads are particularly rich, while shorter-duration spreads are moderately more attractive on a relative basis.

*Orange diamond denotes current value. As of 7/31/2025. Source: Bloomberg L.P. View accessible version of chart.

Market Data

| Yields |

YTM % |

MTD Change |

QTD Change |

YTD Change |

| 3-Mo UST |

4.34 |

0.04 |

0.04 |

0.02 |

| 2-Yr UST |

3.96 |

0.24 |

0.24 |

-0.29 |

| 5-Yr UST |

3.97 |

0.18 |

0.18 |

-0.41 |

| 10-Yr UST |

4.38 |

0.15 |

0.15 |

-0.20 |

| 30-Yr UST |

4.90 |

0.13 |

0.13 |

0.12 |

| Risk Premia |

OAS (bps) |

MTD Change |

QTD Change |

YTD Change |

| Investment Grade Credit |

72 |

-7 |

-7 |

-5 |

| Asset-Backed Securities |

51 |

-6 |

-6 |

7 |

| High Yield |

278 |

-12 |

-12 |

-9 |

As of 7/31/2025. Source: Bloomberg L.P.

Bloomberg Sector/Index Performance (USD)

| |

Duration (yrs.) |

MTD Excess

Return (%) |

YTD Excess

Return (%) |

MTD Total

Return (%) |

YTD Total

Return (%) |

|

Sector

|

| Investment Grade Credit |

6.58 |

0.54 |

0.82 |

0.05 |

4.28 |

| Mortgage-Backed Securities |

5.96 |

0.00 |

0.10 |

-0.40 |

3.81 |

| Asset-Backed Securities |

2.57 |

0.23 |

0.21 |

0.13 |

3.06 |

| High Yield |

2.78 |

0.59 |

1.66 |

0.45 |

5.04 |

| |

Duration (yrs.) |

MTD Excess

Return (%) |

YTD Excess

Return (%) |

MTD Total

Return (%) |

YTD Total

Return (%) |

|

Index

|

| 1-3-Yr Government Credit |

1.79 |

0.03 |

0.15 |

-0.02 |

2.90 |

| Intermediate Government/Credit |

3.67 |

0.14 |

0.29 |

-0.14 |

3.99 |

| U.S. Aggregate |

5.97 |

0.16 |

0.26 |

-0.26 |

3.75 |

As of 7/31/2025. Source: Bloomberg L.P.

Corporate Bond Spreads, 12/31/21-Present*

| |

U.S. Corporate Investment Grade |

1-3 Yr U.S. Corporate |

Long U.S. Corporate |

| Min |

73.58 |

30.08 |

93.29 |

| Median |

96.16 |

58.39 |

126.31 |

| Max |

164.23 |

131.24 |

202.77 |

| Current |

75.71 |

46.27 |

94.12 |

Important Disclosures

This publication is for informational

purposes only. Information contained herein is believed to be accurate, but has

not been verified and cannot be guaranteed. Opinions represented are not

intended as an offer or solicitation with respect to the purchase or sale of

any security and are subject to change without notice. Statements in this

material should not be considered investment advice or a forecast or guarantee

of future results. To the extent specific securities are referenced herein,

they have been selected on an objective basis to illustrate the views expressed

in the commentary. Such references do not include all material information

about such securities, including risks, and are not intended to be

recommendations to take any action with respect to such securities. The

securities identified do not represent all of the securities purchased, sold or

recommended and it should not be assumed that any listed securities were or

will prove to be profitable. Past performance is no guarantee

of future results.

Indices and/or Benchmarks Definitions

PNC Capital Advisors, LLC is a

wholly-owned subsidiary of PNC Bank, National Association, which is a Member

FDIC, and an indirect subsidiary of The PNC Financial Services Group, Inc.

serving institutional clients. PNC Capital Advisors' strategies and the

investment risks and advisory fees associated with each strategy can be found

within Part 2A of the firm's Form ADV.

PNC Capital Advisors, LLC claims

compliance with the Global Investment Performance Standards (GIPS®). A list of

composite descriptions for PNC Capital Advisors, LLC and/or a presentation that

complies with the GIPS® standards are available upon request.

Investments: Not FDIC Insured. No Bank

Guarantee. May Lose Value.

©2025 The PNC Financial Services Group,

Inc. All rights reserved.