Macro

The March headline consumer price index (CPI) report

(released in April) showed a 0.1% month-over-month decline, the first monthly

decrease in nearly five years. Core CPI was also softer, up just 0.1% as travel

related categories exerted downward pressure on inflation. Similarly, the

personal consumption expenditures (PCE) report showed core PCE was unchanged

month-over-month, the tamest pace in five years. Market reaction was muted to

this disinflationary data as they represent the pre-tariff environment.

The April labor report exceeded expectations as

nonfarm payrolls increased 177,000 and the unemployment rate remained at 4.2%.

However, negative revisions from prior months and softer data from other

surveys suggest that worker demand is weakening as employers may be pausing

spending plans until tariff policies become clearer.

2-year U.S. Treasury yields remained below this year's

January peak of 4.38%, ending April at 3.61%. In our view, this reflects

expectations that trade policies will hurt U.S. economic growth later in the

year and force the Federal Reserve to cut interest rates. The market's

expectation for 2025 rate cuts shifted from approximately 75 basis points (bps)

of cuts at the beginning of April, to approximately 100 bps by the end of the

month.

Credit

After a record first quarter, only $15 billion of

investment grade issuance occurred during the first two weeks of April, amid

tremendous market volatility. However, new supply picked up later in the month,

bringing the final monthly tally to more than $100 billion.

Investment grade credit spreads widened 22 bps in the

first six trading days of the month, reaching 111 bps on April 8 as fiscal

policy concerns swept across global financial markets. After the administration

softened trade rhetoric, and paused some tariffs, credit spreads rallied back

to end the month at 100 bps.

Structured

Asset-backed security (ABS) issuance was subdued in

April given broader market volatility. While ABS spreads widened more than

credit, excess returns were less negative given the shorter duration profile.

Following the tariff announcements, the coupon spread

on mortgage-backed securities widened from 20 bps to 164 bps, before retreating

to 159 bps at the end of April.

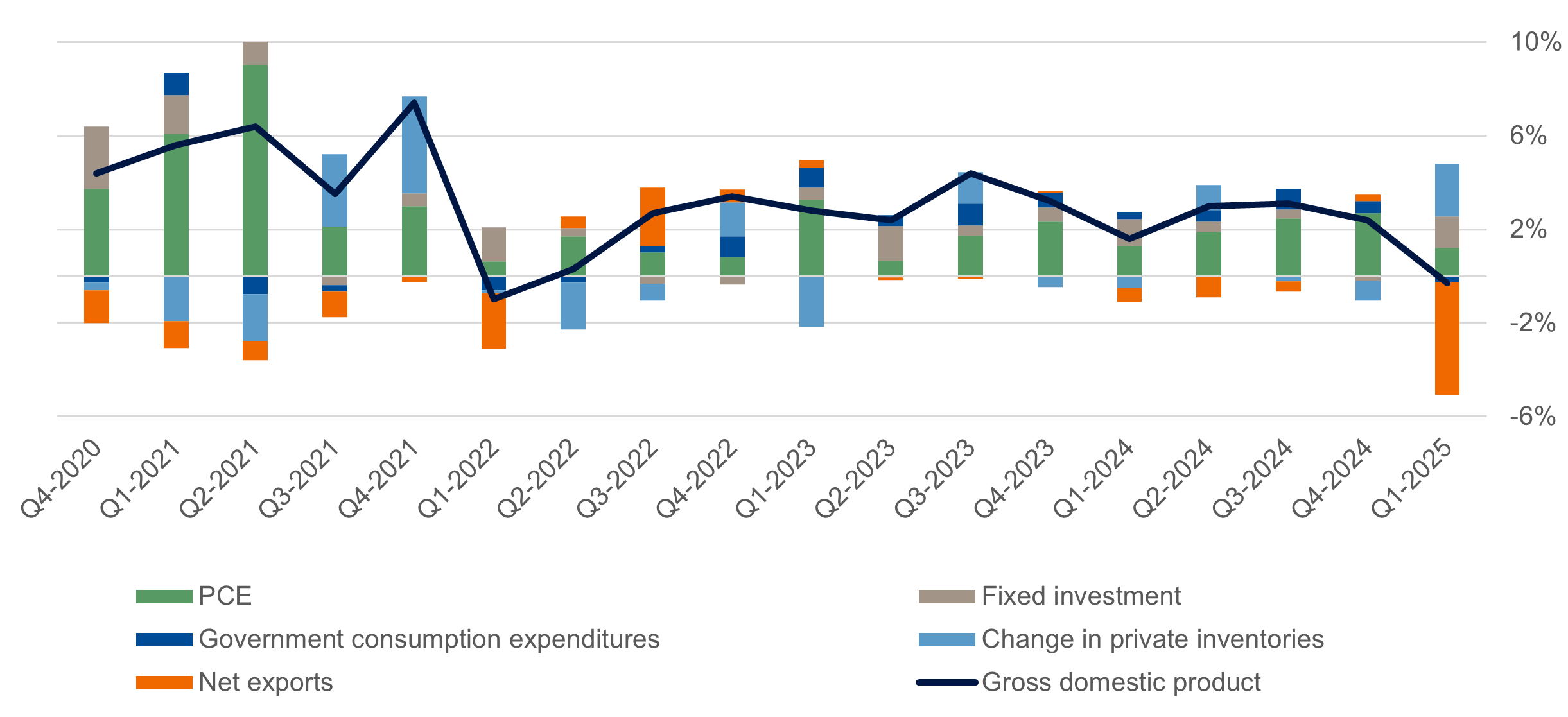

Chart of the Month

Contribution to Real GDP

- U.S. GDP

decreased an annualized 0.3% in the first quarter as net exports subtracted

nearly 500 bps, the most on record.

- Net exports

were influenced by a pre-tariff import surge, which we expect to continue to

obscure economic data reports in the coming months.

As of

4/30/2025. Source: Bloomberg L.P. View accessible version of chart.

Market Data

| Yields |

YTM % |

MTD Change |

QTD Change |

YTD Change |

| 3-Mo UST |

4.29 |

-0.01 |

-0.01 |

-0.03 |

| 2-Yr UST |

3.61 |

-0.28 |

-0.28 |

-0.64 |

| 5-Yr UST |

3.73 |

-0.22 |

-0.22 |

-0.66 |

| 10-Yr UST |

4.16 |

-0.04 |

-0.04 |

-0.41 |

| 30-Yr UST |

4.68 |

0.11 |

0.11 |

-0.10 |

| Risk Premia |

OAS (bps) |

MTD Change |

QTD Change |

YTD Change |

| Investment Grade Credit |

100 |

11 |

11 |

23 |

| Asset-Backed Securities |

74 |

14 |

14 |

30 |

| High Yield |

384 |

37 |

37 |

97 |

As of

4/30/2025. Source: Bloomberg L.P.

Bloomberg Sector/Index Performance (USD)

| |

Duration (yrs.) |

MTD Excess

Return (%) |

YTD Excess

Return (%) |

MTD Total

Return (%) |

YTD Total

Return (%) |

|

Sector

|

| Investment Grade Credit |

6.59 |

-0.55 |

-1.33 |

0.06 |

2.43 |

| Mortgage-Backed Securities |

6.00 |

-0.38 |

-0.47 |

0.29 |

3.35 |

| Asset-Backed Securities |

2.54 |

-0.24 |

-0.53 |

0.49 |

2.03 |

| High Yield |

2.97 |

-1.00 |

-2.15 |

-0.02 |

0.98 |

| |

Duration (yrs.) |

MTD Excess

Return (%) |

YTD Excess

Return (%) |

MTD Total

Return (%) |

YTD Total

Return (%) |

|

Index

|

| 1-3-Yr Government Credit |

1.79 |

-0.04 |

-0.01 |

0.76 |

2.39 |

| Intermediate Government/Credit |

3.69 |

-0.15 |

-0.23 |

0.93 |

3.37 |

| U.S. Aggregate |

6.01 |

-0.25 |

-0.49 |

0.39 |

3.18 |

As of 4/30/2025. Source: Bloomberg L.P.

Contribution to Real GDP (%)

| Category |

Q4 2020 |

Q2 2021 |

Q4 2021 |

Q2 2022 |

Q4 2022 |

Q2 2023 |

Q4 2023 |

Q2 2024 |

Q4 2024 |

| Gross domestic product |

4.40 |

6.40 |

7.40 |

0.30 |

3.40 |

2.40 |

3.20 |

3.00 |

2.40 |

| PCE |

3.74 |

9.04 |

3.00 |

1.71 |

0.81 |

0.65 |

2.33 |

1.90 |

2.70 |

| Fixed investment |

2.66 |

0.99 |

0.53 |

0.35 |

-0.36 |

1.48 |

0.62 |

0.42 |

-0.20 |

| Government consumption expenditure |

-0.27 |

-0.78 |

-0.04 |

-0.27 |

0.90 |

0.48 |

0.61 |

0.52 |

0.52 |

| Change in private inventories |

-0.34 |

-2.00 |

4.14 |

-2.01 |

1.44 |

-0.06 |

-0.47 |

1.05 |

-0.84 |

| Net exports |

-1.38 |

-0.82 |

-0.22 |

0.50 |

0.56 |

-0.11 |

0.09 |

-0.90 |

0.26 |

Important Disclosures

This publication is for informational

purposes only. Information contained herein is believed to be accurate, but has

not been verified and cannot be guaranteed. Opinions represented are not

intended as an offer or solicitation with respect to the purchase or sale of

any security and are subject to change without notice. Statements in this

material should not be considered investment advice or a forecast or guarantee

of future results. To the extent specific securities are referenced herein,

they have been selected on an objective basis to illustrate the views expressed

in the commentary. Such references do not include all material information

about such securities, including risks, and are not intended to be

recommendations to take any action with respect to such securities. The

securities identified do not represent all of the securities purchased, sold or

recommended and it should not be assumed that any listed securities were or

will prove to be profitable. Past performance is no guarantee

of future results.

Indices and/or Benchmarks Definitions

PNC Capital Advisors, LLC is a

wholly-owned subsidiary of PNC Bank, National Association, which is a Member

FDIC, and an indirect subsidiary of The PNC Financial Services Group, Inc.

serving institutional clients. PNC Capital Advisors' strategies and the

investment risks and advisory fees associated with each strategy can be found

within Part 2A of the firm's Form ADV.

PNC Capital Advisors, LLC claims

compliance with the Global Investment Performance Standards (GIPS®). A list of

composite descriptions for PNC Capital Advisors, LLC and/or a presentation that

complies with the GIPS® standards are available upon request.

Investments: Not FDIC Insured. No Bank

Guarantee. May Lose Value.

©2025 The PNC Financial Services Group,

Inc. All rights reserved.