First Quarter Highlights

- U.S. Treasury (UST) yields moved lower across the curve as tariff uncertainty increased downside risks to economic growth.

- The Federal Open Market Committee (FOMC) kept the target fed funds range unchanged at 4.25%-4.50%, while announcing plans to reduce the monthly pace of balance sheet runoff beginning in April.

- The FOMC's Summary of Economic Projections reflected increased risk of higher inflation and diminished expectations for GDP growth in 2025 relative to last quarter's projections. The Committee did not adjust the forecast for the fed funds rate, indicating a cumulative 50 basis points (bps) of rate cuts for the balance of the year.

- As the first quarter progressed, economic data showed signs of deceleration and consumer confidence surveys deteriorated meaningfully, while business surveys underscored uncertainty related to tariff and other policies of the new administration.

- Volatility across financial markets increased during March as investors wrestled with the implications of an intensifying trade war.

- Investment grade corporate issuance set a new first quarter record as companies sought to capitalize on strong investor demand.

- Excess returns were broadly negative across sectors as risk premiums reset from valuations that had begun the year at “priced for perfection” levels.

Duration Positioning

Neutral

Relatively neutral duration positioning given balanced yield and return symmetry.

Credit Sector

Underweight

Expensive valuations support maintaining an underweight allocation from both a contribution to duration and duration times spread perspective.

Structured Products

Overweight

Maintained overweight positions in asset-backed securities (ABS) across strategies. Allocations in agency mortgage-backed securities (MBS) remain modestly overweight within both Aggregate and Non-aggregate styles.

Fiscal Policy Upstages Monetary Policy

Investors' optimistic expectations for economic growth, which stemmed in part from anticipated favorable tax and regulatory policies, were dashed during the first quarter as the administration focused on rapidly implementing significant changes to U.S foreign trade policy. This led to a marked uptick in financial market volatility, which was exacerbated by conflicting messages regarding the extent and timing of the imposition of tariffs against many U.S. trading partners. Additionally, with inflation remaining above the Federal Reserve's 2% target, the prospect of substantial tariffs has raised stagflation concerns across financial markets. Given the challenging environment, investors pivoted to a more cautious stance, resulting in lower UST yields and higher risk premiums.

This flight to quality resulted in a quarterly return of 2.78% for the Bloomberg U.S. Aggregate Index. Investment grade credit spreads increased by 12 bps, resulting in a negative 76 bps of excess returns for the sector (Figure 1). The Utilities sub-sector underperformed both Financials and Industrials, partly due to their longer duration profile but also reflecting idiosyncratic risk related to potential liabilities from the recent wildfires in the state of California. Structured Products proved more resilient; the MBS and ABS sectors realized negative excess returns of 7 bps and 29 bps, respectively (the topline ABS return was also influenced by risks specific to the state of California). Given the risk-off tone, the high yield market unsurprisingly lagged investment grade, with a negative 1.13% excess return.

Figure 1. Sector Comparison

|

Option-Adjusted Spread (bps) |

Excess Returns % |

| Sector |

Current |

Change from Last Quarter |

YTD |

| U.S. Agency |

11 |

(1) |

0.00 |

| U.S. Credit |

89 |

12 |

(0.76) |

| Industrials |

92 |

14 |

(0.94) |

| Utilities |

103 |

21 |

(1.54) |

| Financials |

95 |

13 |

(0.52) |

| Non-corporate Investment Grade |

57 |

2 |

(0.15) |

| U.S. Mortgage-backed Securities |

36 |

(7) |

(0.07) |

| Asset-backed Securities |

60 |

16 |

(0.29) |

| CMBS: ERISA-eligible |

88 |

8 |

(0.07) |

| U.S. Corporate High Yield |

347 |

60 |

(1.13) |

As of 3/31/2025. Source: Bloomberg L.P.

The Dawn of a Manufacturing Renaissance or an Own Goal?

Within weeks of returning to the White House, President Trump announced a barrage of tariffs that sowed confusion and concern among global trade partners. In turn, these announcements created a perplexing environment for markets as they featured mixed signaling regarding the scale, timing and implementation of such policies, and raised questions around the ultimate objectives of the measures.

Many investors had hoped that the primary purpose of announcing imminent tariffs was to create leverage in striking trade deal concessions; however, the administration has highlighted its intention of raising significant revenue from tariffs, which investors have interpreted as implying a more permanent approach. Additionally, the administration's repeated use of rhetoric around the perceived damage of trade deficit suggests that the overarching objective of the tariffs is to dramatically increase domestic manufacturing and production.

Uncertainty built during March as financial markets anticipated the President's April 2 “Liberation Day” event as an opportunity to level set expectations for trade policy. Unfortunately for markets, the tariff rates were much higher than was expected. The White House announced tariff rates that equated to the greater of a 10% flat rate, or a “reciprocal” rate that would apply to trading partners across U.S. manufacturing supply chains.

The market's reaction to these measures was swift, as the announcement was followed by a historic equity market selloff and substantial increase in credit spreads. Many investors cited the myriad of potential negative implications, including retaliatory tariffs, a pullback in capital investment and renewed inflationary pressures, among other impacts that are likely to weigh on domestic and global growth. We are particularly concerned about potential impacts from the weakening of capital flows into the United States, which has benefited from a “safe haven” status in periods of increased uncertainty.

Even with a recent pause in the implementation of the tariffs, we expect market volatility is likely to persist as uncertainty remains elevated, trade negotiations have only just begun and a satisfactory resolution is far from certain.

Fed's Dual Mandate Becoming a Duel

At the March 19 FOMC meeting, the Fed held the fed funds rate steady and maintained its prior projection for a cumulative 50 bps in cuts for the balance of 2025. Acknowledging the potential impact of tariffs, the Fed did raise its forecast for inflation while lowering the forecast for GDP growth in 2025 as the economic data was relatively stable but showed signs of deceleration. In the post-meeting press conference, Chair Jerome Powell suggested that tariffs could have a transitory effect on inflation but acknowledged the Fed would need to wait for final details from the White House.

The FOMC also announced a reduction in the pace of balance sheet runoff by lowering the monthly cap on U.S. Treasury holdings that the Fed would reinvest from $25 billion to just $5 billion. The Fed is typically mindful of its adjustments to the balance sheet as this influences broader liquidity conditions within the financial system. In the near term, we expect the reduction to provide additional flexibility to short-term funding markets given the current impasse around the debt ceiling.

Moving forward, the Fed will be challenged to model both the direct and indirect impacts of tariffs as it relates to how companies pass increased costs on to consumers, along with how to gauge inflation expectations. In recent months, surveys have shown that consumer expectations for inflation have surged (the April 11 University of Michigan Consumer Sentiment Survey indicated consumer's one year inflation forecast reached 6.7%). It is possible that purchasing behaviors have shifted to front-run actual price hikes. This could cloud near-term economic indicators given the temporary impacts of demand being pulled forward. Given these uncertainties, along with already elevated price levels, the risks of a stagflationary environment have risen, in our view.

Ultimately, the Fed's response will depend on how temporary or permanent it assesses the inflation impact of tariffs will be, along with any downside impacts to growth and the labor market. Meeting both the inflation and employment objectives of the Fed's “dueling” mandate could be problematic as traditional monetary policy measures can have conflicting impacts. Boston Fed President Susan Collins confirmed the Fed “would absolutely be prepared” to intervene if market functioning became disorderly, assuaging investor concerns about liquidity issues.

Portfolio Positioning - Defensive Posture Paying Dividends

As we highlighted in last quarter's commentary, historically expensive valuations and a poor symmetry for potential excess returns have led us to an underweight allocation to credit. All of the primary factors that guide our top-down investment outlook present headwinds for credit, with little immediate relief anticipated. Despite the increase in spreads during the first quarter, we believe continued patience is warranted as valuations remain below historical averages. Growing concerns about weaker economic growth and the rising risks of a recession make recent tight spreads across credit look even more expensive.

Corporations have been eager to capitalize on tight spreads as first quarter issuance totaled more than $525 billion, setting a new record to start the year. Investor demand remained quite healthy, and deals were well-subscribed, but those trends began to cool during the second half of March. Focusing on higher-quality issuers, we found some attractive opportunities to participate in new deals that had reasonable pricing. These selective purchases were generally hedged by offsetting sales in order to maintain our desired underweight positioning.

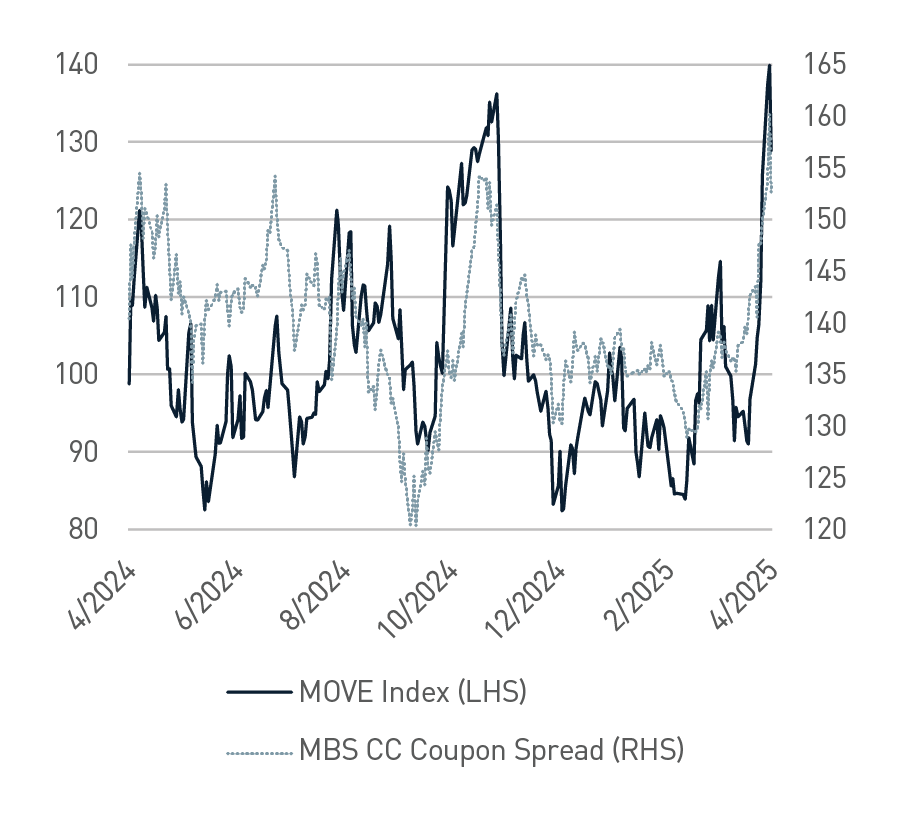

We continue to maintain a positive bias in structured products as we value the portfolio diversification benefits of ABS and MBS. Both sectors outperformed credit in the first quarter and offer reasonable valuations relative to historical norms. Given the increasing odds of a recession this year, we expect these high-quality sectors to remain a key component in portfolios over the course of the year. That said, mortgages will continue to face headwinds should interest rate volatility remain elevated and market liquidity challenged (Figure 2).

Figure 2. ICE BofAML MOVE Index vs. MBS Current Coupon Spread

As of 4/10/2025. Source: Bloomberg L.P.

Outlook: Risk Assets Face a Tariff-ying Wall of Confusion

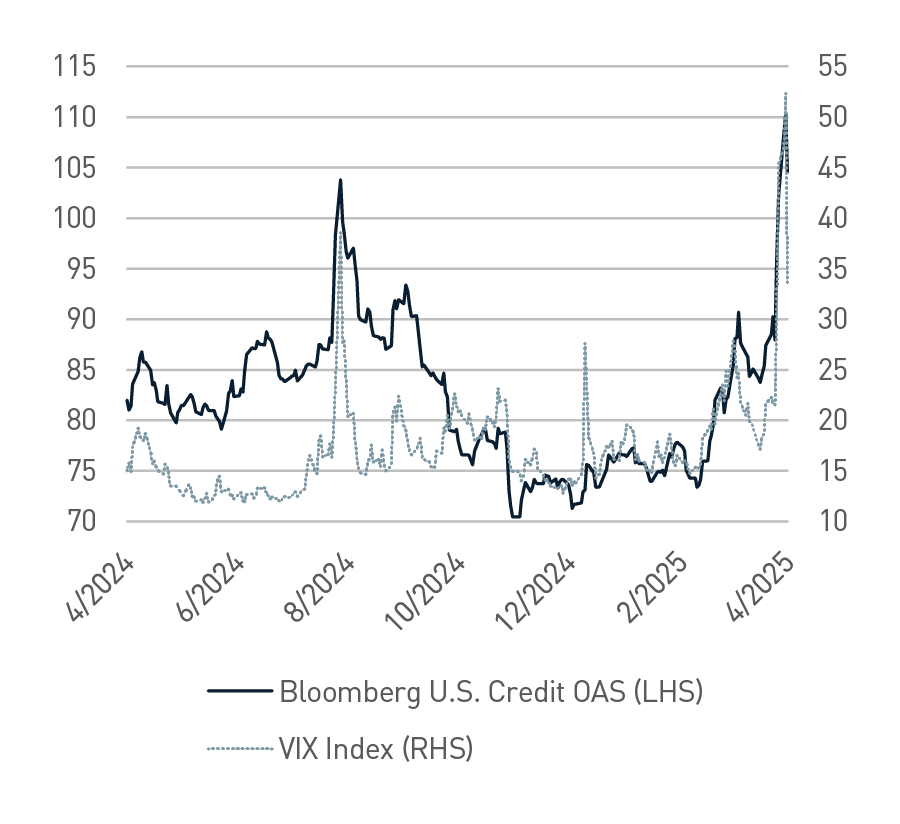

The considerable widening of corporate credit spreads during the early days of April (Figure 3) has presented us with an opportunity to assess increasing portfolio allocations, by capitalizing on dislocations and diminished liquidity. While the new issue market has been largely shutdown in the days following the April 2 tariff announcement, we have been testing levels in the secondary market and selectively adding higher quality positions at attractive spreads. Although valuations are relatively cheaper, we believe they still have a considerable way to go before fully reflecting what is typical in a higher-risk recessionary environment.

Figure 3. Bloomberg U.S. Credit Option-adjusted Spread Index vs. the Cboe Volatility Index®

As of 4/10/2025. Source: Bloomberg L.P.

Fortunately, we believe corporate America is entering this more challenging environment from a strong position — having fortified balance sheets during the pandemic and been supported by a strong earnings tailwind from the last few years. Nonetheless, a long, drawn-out trade war could lead to both supply and demand shocks pressuring margins, sales and ultimately, credit fundamentals. Not all industries or issuers would be impacted equally, a phenomenon which, in our view, highlights the importance of careful risk assessment. As idiosyncratic risk remains elevated, we continue to believe that what an investor does not own in a portfolio could be as consequential as what an investor does own.

While ructions in the U.S. bond market invoked the “Trump put” and brought temporary relief, globally, the outlook remains clouded by escalating geopolitical tensions and the potential for prolonged trade policy uncertainty. In the meantime, the Fed is likely sidelined from immediate policy action given elevated inflation and a relatively healthy labor market. However, negative developments on the latter could present an opportunity for the Fed to act, but we believe this remains unlikely in the near term.

As we likely enter a more protracted period of elevated volatility, we are focused on maintaining flexibility and liquidity in portfolios to capitalize on opportunities when available. In these uncertain times, we believe in the criticality of our disciplined, risk-focused investment approach in the search for a less volatile return experience.

Important Disclosures

Index definitions are available at https://www.pnccapitaladvisors.com/index-definitions/

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

©2025 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE