Macro

The Federal Reserve (Fed) held

interest rates unchanged at its March meeting, while noting its expectations

for lower growth and higher inflation going forward.

In early April, recent U.S.

tariff policy contributed to stagflation concerns, global market disruption and

a steepening yield curve, which ultimately reflected slowing growth

expectations. As of April 3, the Federal Reserve Bank of Atlanta's GDPNow model

estimate is -2.8% for the first quarter.

Market pricing for Fed rate cuts

has shifted materially in response to the early April tariff announcements;

currently, approximately 100 basis points (bps) of cuts are discounted for the

balance of 2025. Despite the increased volatility and market expectations for

cuts, Fed Chair Jerome Powell noted the Federal Open Market Committee is “well

positioned to wait for greater clarity before considering any adjustments to

our policy stance.”

Credit

Primary markets were active

during March as issuers took advantage of receptive buyer demand prior to the

increased volatility at month-end. Despite the month-end slowdown, investment

grade issuance during the first quarter set a record at $531 billion.

Following the record pace of

issuance in the first quarter, new supply is expected to slow during the month

of April to an estimated $120 billion in investment grade supply.

Investment grade spreads closed

the month of March at 89 bps; however, in early April, spreads continued to

widen, closing the week of April 4 at 103 bps due to tariff volatility and

economic uncertainty. Correspondingly, the ICE BofAML MOVE Index closed at 125,

its highest level since November 2024.

Structured

Asset-backed security spreads

increased during March but recouped some of the widening as issuance slowed and

all-in levels attracted buyers. Auto-backed deals comprised approximately 51%

of new issue volume.

Despite renewed interest rate

volatility, the mortgage-backed sector has outperformed credit year-to-date

given the growing risk-off tone.

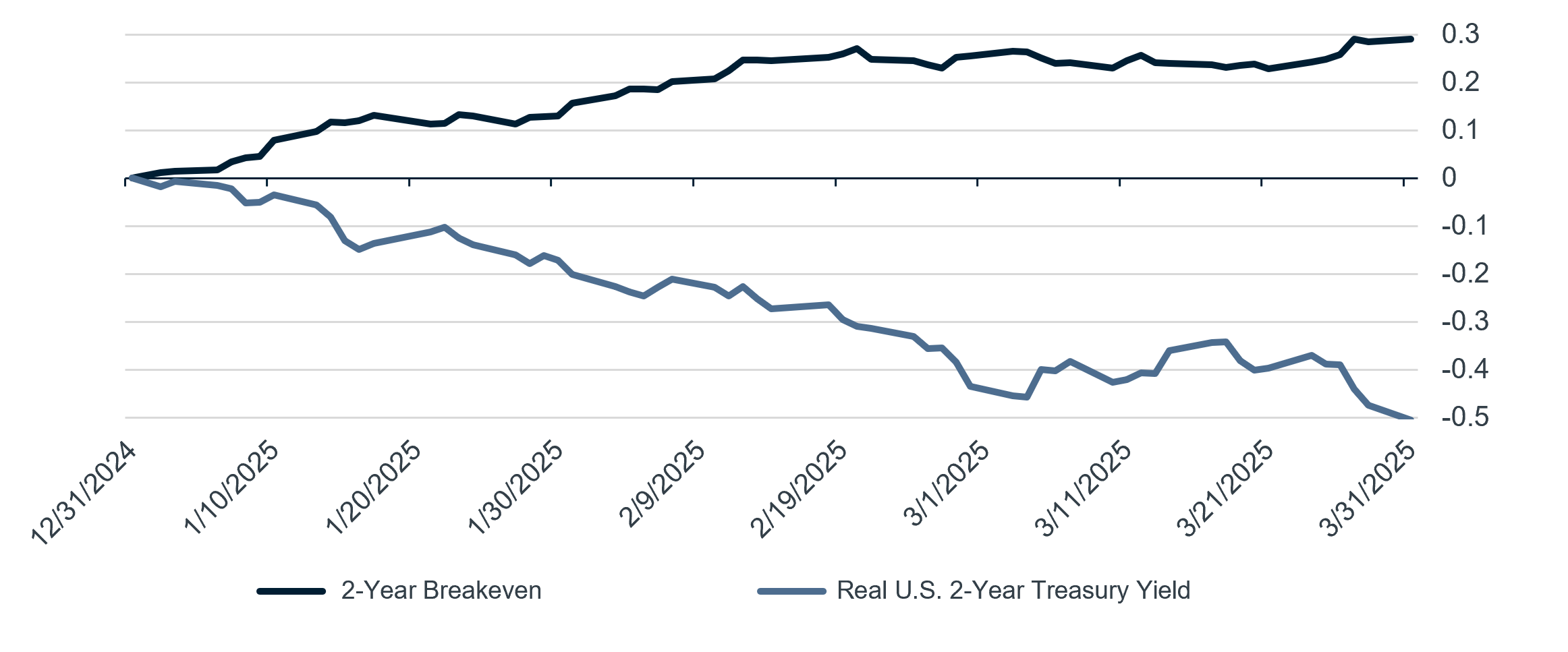

Chart of the Month

U.S.

2-Year Breakeven and Real U.S. Treasury Yield* (%)

- Year-to-date

real yields have plummeted, while breakeven rates on Treasury

Inflation-Protected Securities have increased.

*Normalized as of 12/31/2024. As of 3/31/2025. Source: Bloomberg L.P.

Market Data

| Yields |

YTM % |

MTD Change |

QTD Change |

YTD Change |

| 3-Mo UST |

4.30 |

0.00 |

-0.02 |

-0.02 |

| 2-Yr UST |

3.89 |

-0.11 |

-0.36 |

-0.36 |

| 5-Yr UST |

3.95 |

-0.07 |

-0.43 |

-0.43 |

| 10-Yr UST |

4.21 |

0.00 |

-0.37 |

-0.37 |

| 30-Yr UST |

4.57 |

0.08 |

-0.21 |

-0.21 |

| Risk Premia |

OAS (bps) |

MTD Change |

QTD Change |

YTD Change |

| Investment Grade Credit |

89 |

6 |

12 |

12 |

| Asset-Backed Securities |

60 |

10 |

16 |

16 |

| High Yield |

347 |

67 |

60 |

60 |

As of 3/31/2025. Source: Bloomberg L.P.

Bloomberg Sector/Index Performance (USD)

| |

Duration (yrs.) |

MTD Excess

Return (%) |

YTD Excess

Return (%) |

MTD Total

Return (%) |

YTD Total

Return (%) |

|

Sector

|

| Investment Grade Credit |

6.62 |

-0339 |

-0.76 |

-0.24 |

2.36 |

| Mortgage-Backed Securities |

5.90 |

-0.27 |

-0.07 |

-0.02 |

3.06 |

| Asset-Backed Securities |

2.56 |

-0.18 |

-0.29 |

0.23 |

1.53 |

| High Yield |

3.01 |

-1.51 |

-1.13 |

-1.02 |

1.00 |

| |

Duration (yrs.) |

MTD Excess

Return (%) |

YTD Excess

Return (%) |

MTD Total

Return (%) |

YTD Total

Return (%) |

|

Index

|

| 1-3-Yr Government Credit |

1.78 |

-0.01 |

0.03 |

0.46 |

1.63 |

| Intermediate Government/Credit |

3.67 |

-0.06 |

-0.08 |

0.44 |

2.42 |

| U.S. Aggregate |

6.01 |

-0.18 |

-0.23 |

0.04 |

2.78 |

As of 3/31/2025. Source: Bloomberg L.P.

Important Disclosures

This publication is for informational

purposes only. Information contained herein is believed to be accurate, but has

not been verified and cannot be guaranteed. Opinions represented are not

intended as an offer or solicitation with respect to the purchase or sale of

any security and are subject to change without notice. Statements in this

material should not be considered investment advice or a forecast or guarantee

of future results. To the extent specific securities are referenced herein,

they have been selected on an objective basis to illustrate the views expressed

in the commentary. Such references do not include all material information

about such securities, including risks, and are not intended to be

recommendations to take any action with respect to such securities. The

securities identified do not represent all of the securities purchased, sold or

recommended and it should not be assumed that any listed securities were or

will prove to be profitable. Past performance is no guarantee

of future results.

Indices and/or Benchmarks Definitions

PNC Capital Advisors, LLC is a

wholly-owned subsidiary of PNC Bank, National Association, which is a Member

FDIC, and an indirect subsidiary of The PNC Financial Services Group, Inc.

serving institutional clients. PNC Capital Advisors' strategies and the

investment risks and advisory fees associated with each strategy can be found

within Part 2A of the firm's Form ADV.

PNC Capital Advisors, LLC claims

compliance with the Global Investment Performance Standards (GIPS®). A list of

composite descriptions for PNC Capital Advisors, LLC and/or a presentation that

complies with the GIPS® standards are available upon request.

Investments: Not FDIC Insured. No Bank

Guarantee. May Lose Value.

©2025 The PNC Financial Services Group,

Inc. All rights reserved.