Fourth Quarter Highlights

- The Federal Reserve (Fed) continued easing policy with 25-basis point (bp) cuts at both Federal Open Market Committee (FOMC) meetings during the fourth quarter, bringing the target fed funds range to 4.25%-4.50%.

- While yields on very short-dated U.S. Treasury (UST) bills moved lower in unison with the fed funds rate, yields on USTs with maturities beyond one-year moved substantially higher. This steepening trend across the UST curve persisted for much of the second half of 2024.

- The FOMC's December projections indicated 50 bps of cuts in 2025 and another 50 bps during 2026. While this represents a less aggressive pace of easing than what was illustrated in the September projection, markets are currently discounting just 25 bps of cuts both this year and next.

- Economic data remained resilient as strong consumer spending continued to drive growth. Progress on inflation stalled during the quarter, highlighting the challenging dynamics the Fed faces in lowering inflation to its 2% target.

- Following the election, financial markets had a generally optimistic growth outlook due to anticipated regulatory and tax policies, which has been somewhat offset by concerns related to trade, deficits and inflation expectations.

- Investment-grade corporate issuance during the quarter capped off a robust year; 2024 supply came in second only to the record pace of 2020.

- Some of the post-election rally in Credit reversed during the second half of December, but spreads ended the quarter tighter overall.

Duration Positioning

Neutral

Relatively neutral duration positioning given balanced yield and return symmetry.

Credit Sector

Underweight

Slight preference for Financials relative to Industrials but underweight Credit overall in both contribution to duration and duration times spread.

Structured Products

Overweight

Maintained overweight positions in Asset-backed Securities (ABS) across strategies. Allocations in Agency Mortgage-backed Securities (MBS) remain modestly overweight within both Aggregate and Non-aggregate styles.

Laissez-faire Risk Markets Confront a More Cautious Fed

In atypical fashion, yields across much of the UST curve moved higher during the fourth quarter despite policy rate cuts at consecutive FOMC meetings. Market movements were likely the result of strong economic data, elevated inflation readings and expectations related to the incoming administration's fiscal policy objectives. Riskier asset classes continued to outperform through year end as investors appeared generally optimistic that conditions will remain favorable for economic growth in 2025.

The jump in yields resulted in a quarterly return of -3.06% for the Bloomberg US Aggregate Index, limiting the full-year return to 1.25%. Investment-grade credit spreads narrowed 7 bps, which generated 72 bps of positive excess returns for the sector (Figure 1). Structured products were mixed; the MBS sector posted modestly negative excess returns while ABS outperformed resoundingly. The High Yield sector had yet another strong quarter, allowing it to outperform investment grade every quarter this year.

Figure 1. Sector Comparison

Spread compression led to positive excess returns across most sectors

|

Option-Adjusted Spread (bps) |

Excess Returns % |

| Sector |

Current |

Change from Last Quarter |

3 Month |

YTD |

| U.S. Agency |

12 |

(4) |

0.09 |

0.38 |

| U.S. Credit |

77 |

(7) |

0.72 |

2.23 |

| Industrials |

78 |

(9) |

0.89 |

2.07 |

| Utilities |

82 |

(10) |

1.16 |

3.40 |

| Financials |

82 |

(8) |

0.62 |

2.88 |

| Non-corporate Investment Grade |

55 |

1 |

- |

0.72 |

| U.S. Mortgage-backed Securities |

43 |

1 |

(0.13) |

0.37 |

| Asset-backed Securities |

44 |

(20) |

0.61 |

1.53 |

| CMBS: ERISA-eligible |

80 |

(13) |

0.66 |

2.80 |

| U.S. Corporate High Yield |

287 |

(8) |

1.17 |

5.02 |

As of 12/31/2024. Source: Bloomberg L.P.

Fed Update — More Questions than Answers

The notable deterioration in labor markets during the summer was a primary consideration when the FOMC initiated the easing cycle in September with a somewhat surprising 50-bp cut in the fed funds rate. The employment reports that followed early in the fourth quarter were clouded by severe weather events and strikes, creating a challenging environment to assess ongoing trends.

Despite the lack of visibility, the FOMC proceeded with additional 25 bp cuts in November and December; meanwhile, its guidance and rhetoric became slightly more hawkish due to sticky inflation, a resilient economy and a bounce back in employment data. Revised forecasts for 2025 illustrated both an improved outlook for the unemployment rate and less progress on inflation than the prior release in September. However, financial markets focused on the higher projected forecast for the fed funds rate. The median forecasted rate showed just two additional cuts over the course of 2025 compared to four previously. In the post-meeting press conference, Chair Jerome Powell acknowledged that despite policy still being restrictive, the committee would have a more cautious approach moving forward as downside risks appear to have diminished.

Further complicating the Fed's outlook are the highly unknown fiscal policy objectives of the incoming administration. Significant potential changes to trade, regulatory, tax and immigration policies highlight the Republican agenda, and each of these initiatives could have material impacts on the economic outlook. Given this uncertainty, we expect the Fed to take its time evaluating the changing situation. Additionally, because the fed funds rate has been lowered by a full percent and the tone of unemployment has improved, we believe markets expect a wait-and-see approach. In fact, upon the release of the December employment report in early January, which was significantly stronger than anticipated, market pricing pushed out expectations for the next rate cut well into the back half of 2025.

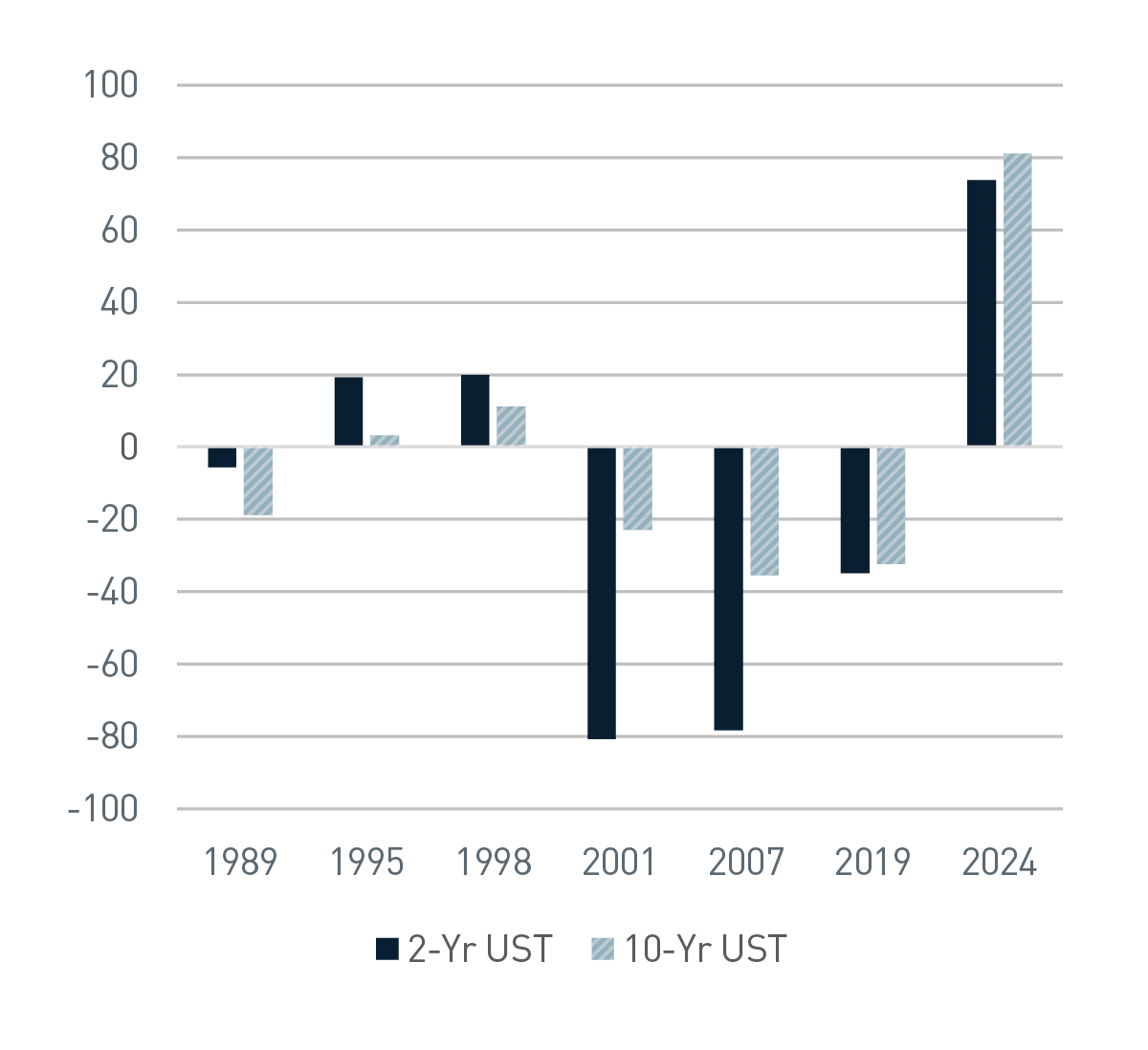

These evolving circumstances have also had significant impacts on the shape of the yield curve, as continued steepening has resulted in a more normalized, upwardly sloping curve. What has been particularly noteworthy is the degree that yields have risen following the initiation of Fed cuts. Historically, the Fed has begun cutting cycles in response to heightened fears of recession as opposed to a recalibration of policy. Figure 2 illustrates the uniqueness of this current environment in which the Fed is easing policy while pockets of inflation persist. Sizeable deficits and increased future borrowing

needs further complicate the cloudy fiscal policy situation.

Figure 2. 3-month Change in Yield Following First Fed Rate Cut in Cycle, bps

The yield response to the current Fed cutting cycle is unique

As of 12/31/2024. Source: Bloomberg L.P.

Credit Risk Premiums Remain Inflated; Structured Products Still Offers Value

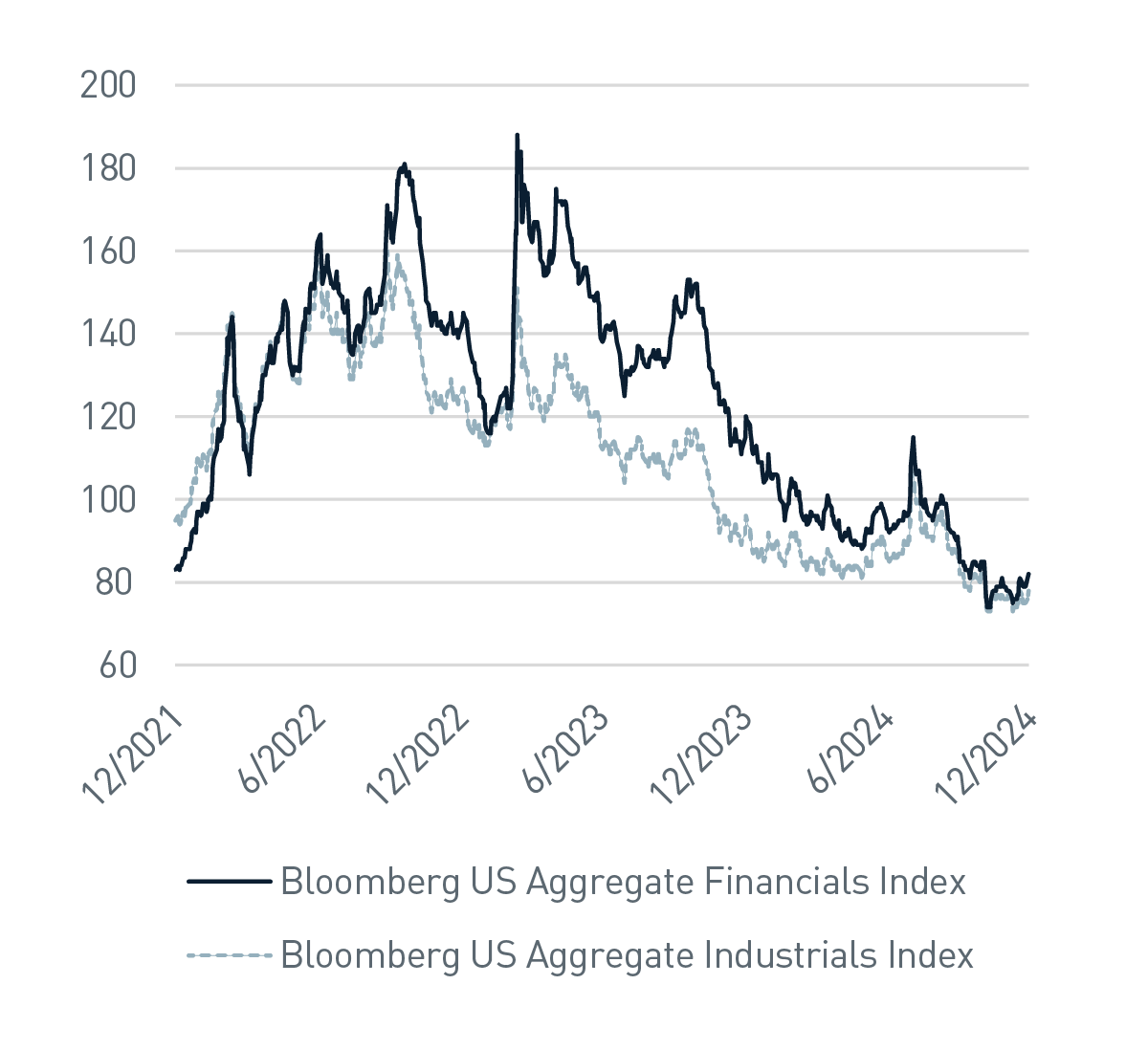

As we have highlighted in recent quarters, valuations within Corporate Credit have been expensive for much of the past year (see our commentary, Credit Keeps on Truckin', Mortgages Ride the Struggle Bus). Shortly after the election, credit spreads rallied to new post-financial-crisis lows before reversing course and modestly widening back to mid-October levels. Given the limited potential we see for spread compression from current levels, we have continued to reduce credit exposure across strategies and are now modestly underweight relative to benchmarks on a contribution-to-duration basis. Earlier in the year, we reduced positions primarily within the Industrials sector as valuations were more favorable in Financials. That relative advantage steadily narrowed over the course of 2024 and prompted some opportunistic risk reduction in the banking sector (Figure 3).

Figure 3. Average Option-adjusted Spread, bps

The relative advantage offered by Financials narrowed during the second half of 2024

As of 12/31/2024. Source: Bloomberg L.P.

As we await better opportunities to increase exposure in Credit, we maintain overweight allocations in Structured Products, where valuations remain more compelling. While the ABS sector had a strong fourth quarter, with spreads narrowing 20 bps, we maintain a favorable bias. Our ABS allocations are confined to AAA-rated issuers with average lives primarily inside of 3 years, making the sector a defensive alternative to lower-rated, short-duration Credit.

MBS performance continues to be challenged by the dynamic interest rate environment, leaving valuations reasonably attractive relative to historical averages. Given the sector's high credit quality and our positioning in securities with less prepayment risk, we maintain our overweight allocations as we believe the sector is one of the few areas offering sufficient compensation for its underlying risks. While interest rate volatility may continue to be a headwind, the steepening yield curve should be beneficial as it has historically provided a favorable environment for MBS.

Outlook: Budget Tail Wags the Dog

We again start the year with considerable headwinds from the four primary factors that guide our market outlook — fiscal policy, monetary policy, inflation and volatility. The incoming administration's policy priorities will take center stage, with objectives around taxes, spending and trade potentially having meaningful downstream impacts on other macro factors that guide our risk positioning. Monetary policy has already shifted into a more cautious mode given fiscal policy uncertainties as well as continued strength in economic data. Inflation remains above the 2% policy target, with its stalled progress evident in both the second and fourth quarters of last year. Finally, volatility in both equity and fixed income markets is creeping back up as the initial ebullience of higher growth expectations ahead of the election is being met with the reality of budget considerations and the costs to finance growing deficits.

Our defensive outlook continues to be primarily informed by expensive valuations as opposed to weakening economic or corporate fundamentals. We believe a patient approach is appropriate as pockets of financial markets appear complacent to stretched valuations. The resiliency of the U.S. economy amid restrictive monetary policy has been remarkable over the past couple of years. However, that has not been without periods of notable risk-off events, both domestically and abroad.

Fortunately for fixed income investors, the current environment remains favorable with attractive yields that now outpace cash alternatives. Importantly, we believe the inflation-adjusted yield on broad fixed income indices is compelling and creates a better symmetry of outcomes going forward; the yield to worst on the Bloomberg US Aggregate Index is approximately 5.1% as of this writing, which is equal to the average level over the last 40 years! Over the same period, the index generated an average annual return of 5.85%. Given the recent selloff in USTs, we believe investors can capitalize on the environment without having to meaningfully increase credit risk as much of the market's overall yield is attributable to risk-free rates, rather than spreads. Should further progress on inflation prove elusive, or should new fiscal measures exacerbate the situation, we believe it's likely that risk premiums react negatively.

Important Disclosures

Index definitions are available at https://www.pnccapitaladvisors.com/index-definitions/

This publication is for informational purposes only. Information contained herein is believed to be accurate, but has not been verified and cannot be guaranteed. Opinions represented are not intended as an offer or solicitation with respect to the purchase or sale of any security and are subject to change without notice. Statements in this material should not be considered investment advice or a forecast or guarantee of future results. To the extent specific securities are referenced herein, they have been selected on an objective basis to illustrate the views expressed in the commentary. Such references do not include all material information about such securities, including risks, and are not intended to be recommendations to take any action with respect to such securities. The securities identified do not represent all of the securities purchased, sold or recommended and it should not be assumed that any listed securities were or will prove to be profitable. Past performance is no guarantee of future results.

PNC Capital Advisors, LLC claims compliance with the Global Investment Performance Standards (GIPS®). A list of composite descriptions for PNC Capital Advisors, LLC and/or a presentation that complies with the GIPS® standards are available upon request.

PNC Capital Advisors, LLC is a wholly-owned subsidiary of PNC Bank N.A. and an indirect subsidiary of The PNC Financial Services Group, Inc. serving institutional clients. PNC Capital Advisors’ strategies and the investment risks and advisory fees associated with each strategy can be found within Part 2A of the firm’s Form ADV, which is available at https://pnccapitaladvisors.com.

©2025 The PNC Financial Services Group, Inc. All rights reserved.

FOR INSTITUTIONAL USE ONLY

INVESTMENTS: NOT FDIC INSURED-NO BANK GUARANTEE – MAY LOSE VALUE